Detailed Components of a Project Finance Model Structure

Hands on Detailed Components of a Project Finance Model Structure

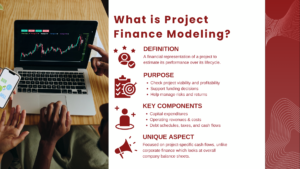

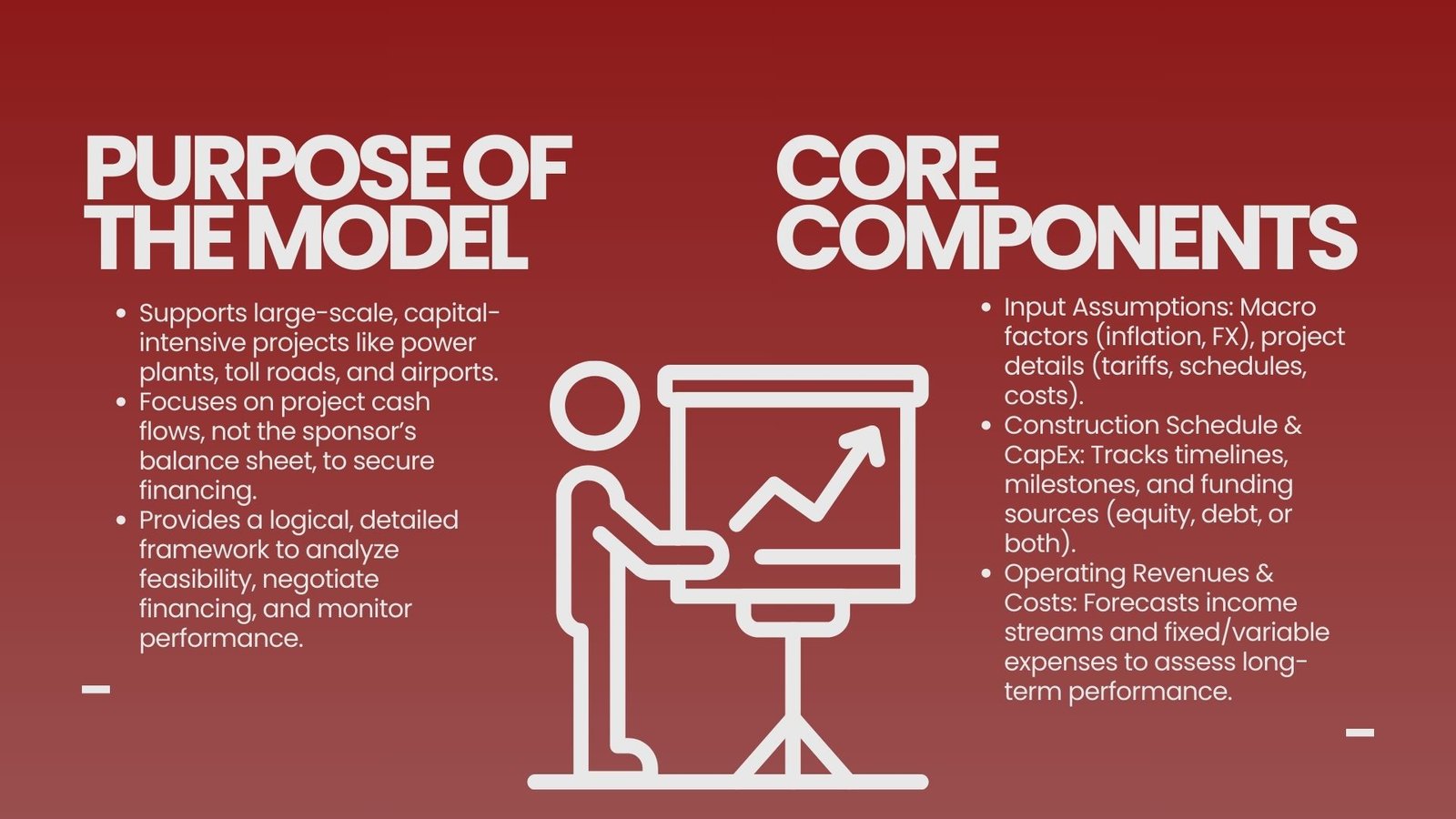

Project finance comprises one of the more niche sectors of corporate and infrastructure finance, offering a vehicle with which to finance capital-intensive and large-scale projects, such as power plants, toll roads, airports, mining projects and environmentally-engaged alternative energy plants. Project finance in contrast to conventional corporate finance is based on rigorous financial structuring of future cash flows of the project itself in order to raise the debt and equity capital with very minimal or no access to the sponsor’s balance sheets.

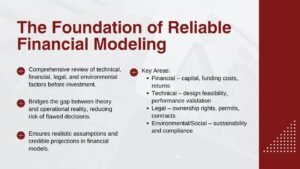

The exclusive design demands a complex and a very detailed financial model to determine feasibility, assist the negotiation time, finance to gain funds and the continuing performance. An effective project financing plan simplifies complicated confusion into an orderly, logical and comprehensible arrangement of economic statements and computations which allow the investors, financiers and project sponsors to make right choices.

The aspects of a project finance model are encompassed and each segment plays a certain role to turn project assumptions into meaningful results, like cash flows, debt repayment schedules, and the returns of investors. Although the structure and intricacy of the model would depend on the sector of the project, jurisdiction, and economy of arrangement, some of its major vital parts are universal. An individual who will develop, analyze, or even audit various models is required to understand these components.

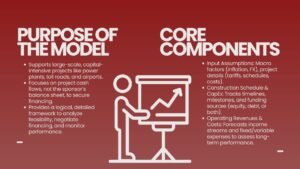

1. Input Assumptions and Drivers

All project finance models are based upon a series of input assumptions. These assumptions become the foundation of the rest of the model, and most usually these are grouped together in a well structured and clearly defined section of the model called the inputs so as to provide easy update and scenario checking possibilities. The categories of events into which input assumptions apply are very broad, including macroeconomic factors like inflation rates and exchange rates, and project-specific factors e.g. building schedules, working capacity, tariffs and cost estimates.

At the initial development phases of a project, a number of these assumptions can be found in feasibility studies, engineering documents, and in market studies. With the development of the project, these inputs are refined to a more precise and binding information like signed contracts, committed construction cost and controlled financing terms. Sensitivity analysis is quite commonly done on the model to determine the sensitivity of any given variable to change in financial statements considering the fact the reliability of assumptions made in the model determines the accuracy of the entire model.

2. Construction Period Costs and Schedule

One of the most crucial stages of a project finance model is the construction phase since it decides when the cash outflows can occur before the project begins to earn an income. The construction duration stipulates how long the build will take, key milestones and payment rates to contractors and equipment providers. The model also contains the capital expenditure (CapEx) budget in line with the schedule, though the budget can further be classified into categories (e.g. civil works, machinery, engineering, and contingency reserves).

It is essential to properly model the costs of construction as any overruns or delays can be very detrimental to debt drawdown and interest during construction (IDC) in addition to overall financial feasibility of the overall debt. The model should also consider the funding of these costs i.e. will it be by equity injections, debt drawdown or a combination of both and there should be clear connections of this part of the model with the sources and uses of funds statement.

3. Operating Revenues and Cost Structure

When the project is at commercial operation, operational revenues and cost modeling is therefore the center of focus. The revenue angle is banked on the character of the project. As an example, the revenue of a power plant could be determined by a power purchase agreement (PPA) fixed tariff rate and indexed adjustments, and a toll road revenue would be dependent on the projections about the traffic volumes and toll rates. One should differentiate the contracted revenue that offers more certainty and the merchant revenue that is subjected to the risks in the market.

Total costs of operation can be classified as fixed costs as well as variable. Variable costs, costs that fluctuate with alterations in production or service, include fuel, raw materials, or that based on usage, e.g., maintenance contracts and salaries are relatively constant with time, are referred to as fixed costs. The working capital requirements such as accounts receivable and accounts payable are also captured in the operating section of the model as the differences in timing of the collecting or receiving revenues or incurring expenses or paying them.

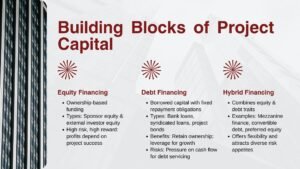

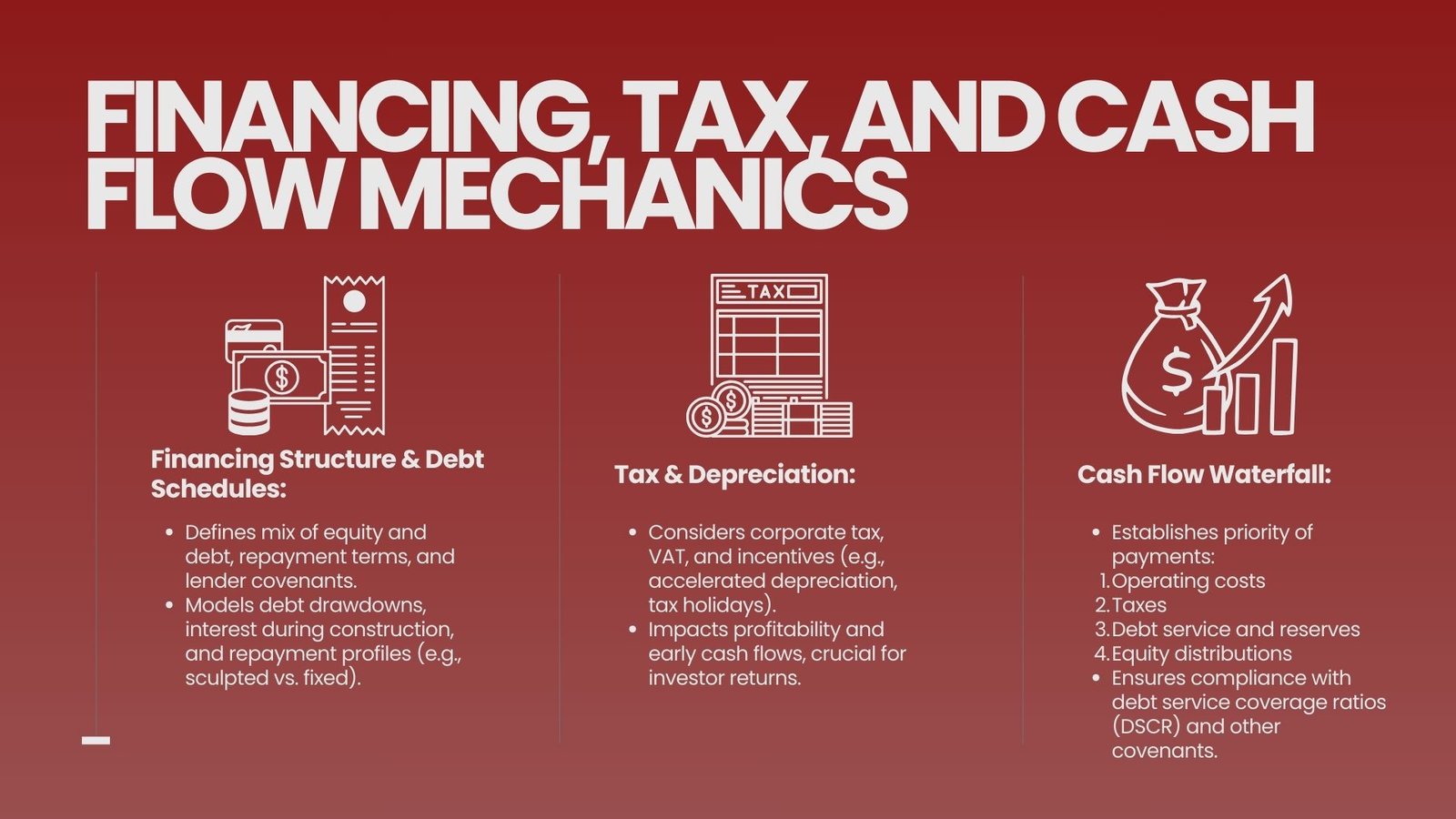

4. Financing Structure and Debt Schedules

One of the characteristics of a project finance model is the financing structure. It identifies the combination between equity and debt and their respective sources together with the terms and conditions of repayment. Senior loans, mezzanine debt, and subordinated loans all fall into the category of project financing debt, and they each have their priorities within the terms of repayment and interest rates as well as covenant requirements. The model should then compute the debt service payments according to amortization as agreed which might be sculpted such that it fits the cash flows or in a fixed repayment pattern.

A detailed debt schedule would have staff concerning drawdowns on construction, interest percentages (as to whether interest is capitalized prior to the operations) repay reimbursement schedule and if any refinancing was anticipated. Lender requirements to the establishment of proper debt service reserve accounts (DSRAs) resulting in timely repayment is also modeled in this section. Since lenders tie their faiths so much on the debt service coverage ratio (DSCR) and other credits factors, the section on financing structure is closely related with covenant compliance analysis.

5. Tax and Depreciation Calculations

Taxes may determine greatly whether a project will be viable or not and the model should take into account local tax laws as well as project-related incentives. Typical taxation concepts involve corporate income tax, interest or dividend withholding tax, and indirect taxation i.e. VAT or sales tax. Depreciation schedules are also significant because they decrease taxable profits and alter accounting earnings without any influence on the cash flow. Understanding depreciation methods for finance is essential in this context.

In other instances, there are accelerated depreciation or tax holidays which can help in improving the early year cash flows and thus making the project more appealing to the investors. The model covering the tax section also covers the treatment of the losses carried forward, thin capitalisation rules and other rules peculiar to the jurisdiction which impact financial results.

6. Cash Flow Waterfall

One characteristic of project finance is the cash flow waterfall or prioritization of allocation of the available cash to disparate uses. The waterfall depicts that debt repayment should have the priority over equity distributions where the lenders will be repaid first before equity sponsors get returns to the project. The general pattern of payment is operating cost, taxes, debt expense, reserve accounts funding, and lastly distributions to equity investor.

To calculate the timing and amount required when the waterfall makes any investments, it is important to model the waterfall correctly so that both the debt and equity participants obtain the required returns. The waterfall also reflects the lender-required covenants; that is, the minimum levels of DSCR will be maintained prior to the distributions. The violation of any of these covenants would provoke a restriction of equity payouts and this part will be vital to the sponsors and the financiers.

7. Financial Statements Integration

To get a detailed picture of the performance of the project, its core financial statements should be prepared, which are the income statement, the balance sheet and the cash flow statement. Under the project finance model, all these statements are integrally drafted, i.e. change in one statement will automatically be reflected in other statements. To use an example, the increase or decrease in CapEx will change the balance sheet in terms of among others, value of assets, the income statement in terms of depreciation and the cash flow statement as far as outflow of investment is concerned.

Integration brings internal consistency and enables the stakeholders to see how the operational and financial decisions impact upon the overall financial situation of the project. Such an integration is also necessary in performing sensitivity and scenario analyses since it makes all components of the model react in a synchronized manner in case of changes in assumptions. This approach also helps stakeholders effectively analyze company performance using financial statements for more accurate insights.

8. Sensitivity and Scenario Analysis

Sensitivity and scenario analysis is crucial in the project finance modeling process considering that any large-scale project is a risky venture at heart. Sensitivity analysis is used to check how the key measures of this project, such as DSCR, equity IRR, and project NPV change depending on the fluctuations in individual variables e.g. interest rates, construction costs, or demand levels. Scenario analysis, however, assesses the resulting impact of two or more changes, e.g. increasing the delay of construction and a drop in tariffs.

The set of analyses enables lenders and sponsors to notice the highest risks and organize mitigation provisions. As an example, DSCR may not be acceptable until lenders order extra reserve accounts or increased equity contributions should there be moderate drops in demand that force DSCR below the acceptable levels that were factored by the model.

9. Outputs and Key Performance Indicators

The model of project finance would end with the outputs that are to inform the decision-making. The performance measures, which include equity internal rate of return (IRR), project IRR, net present value (NPV), and DSCR give a succinct report of the project appeal and bankability. Commonly these outputs can be displayed in a dashboard view to easily reference with the option to drill down into supporting details.

The lenders are concerned more with the credit metrics whereas the sponsors are concerned more with returns on equity. Regulators to the extent they are involved also may demand certain performance measures that are to be monitored throughout the project life. An output section should clearly indicate to all the stakeholders necessary information concerning the financial strength of the project.

Conclusion

The models relating to the project finance are a complex intertwined system which transforms the assumptions into the full representation of the financial feasibility of a project. Tracing the input assumptions to the KPIs that were defined, each of the sections is vital in reflecting the magnitude of big, capital-intensive projects. An effective model can increase investment choices as well as provide a dynamic management tool at all times during the life cycle of the project provided it is transparent, flexible and accurately represents the known costs.

Required in practice would be not only the technical skills on how to model, but also the thorough comprehension of the commercial, contractual and financial reality of the project. Being able to balance detail against clarity, and to make sure the model is capable of sustaining scrutiny by lenders, sponsors and auditors is what separates a genuinely useful project finance model and a mere forecasting tool. To the professionals engaged in planning and analysing such projects, understanding the elements of financial model is a mandatory aspect of making the project, not only viable financially but also environmentally and socially viable in the long run.