Project Finance Modeling Best Practices for Debt Equity WACC and NPV

Understanding Project Finance Modeling Best Practices for Debt Equity WACC NPV

Project finance is a form of specialized corporate finance, concerned with raising capital (rarely all-equity financed) to finance long-term infrastructure, industrial, and public service projects. Instead of only having a balance sheet of a company, the project finance facilities generally rely on cash flows of the project where the cash flows provide the main source of repayment. In a bid to assess these investments successfully, financial experts will need to come up with models that are strong, and which will require inclusion of the following components; structuring of debt, equity funding, weighted average cost of capital (WACC) and net present value (NPV).

It is critical to understand how these elements interrelate in a project finance model whose main objective is to provide financial viability of the project and to make the investment to attract stakeholders. Professionals seeking to enhance these skills can benefit from the Best Project Finance Modeling Training Singapore to gain practical knowledge and industry-relevant expertise.

The Role of Debt in Project Finance Models

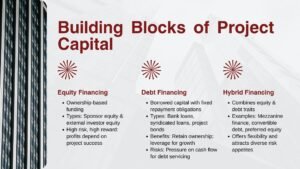

In terms of its application, debt is a central figure in project finance as it enables the developer to finance a big project without having to raise all the financing at once. The amount of debt financing included on the funding mix can be large, it may surpass 70 percent of the total project cost. High leverage can be achieved due to the fact that project finance debt is often secured by the assets of the project, its contract and revenues to come, instead of the balance sheet of the sponsor.

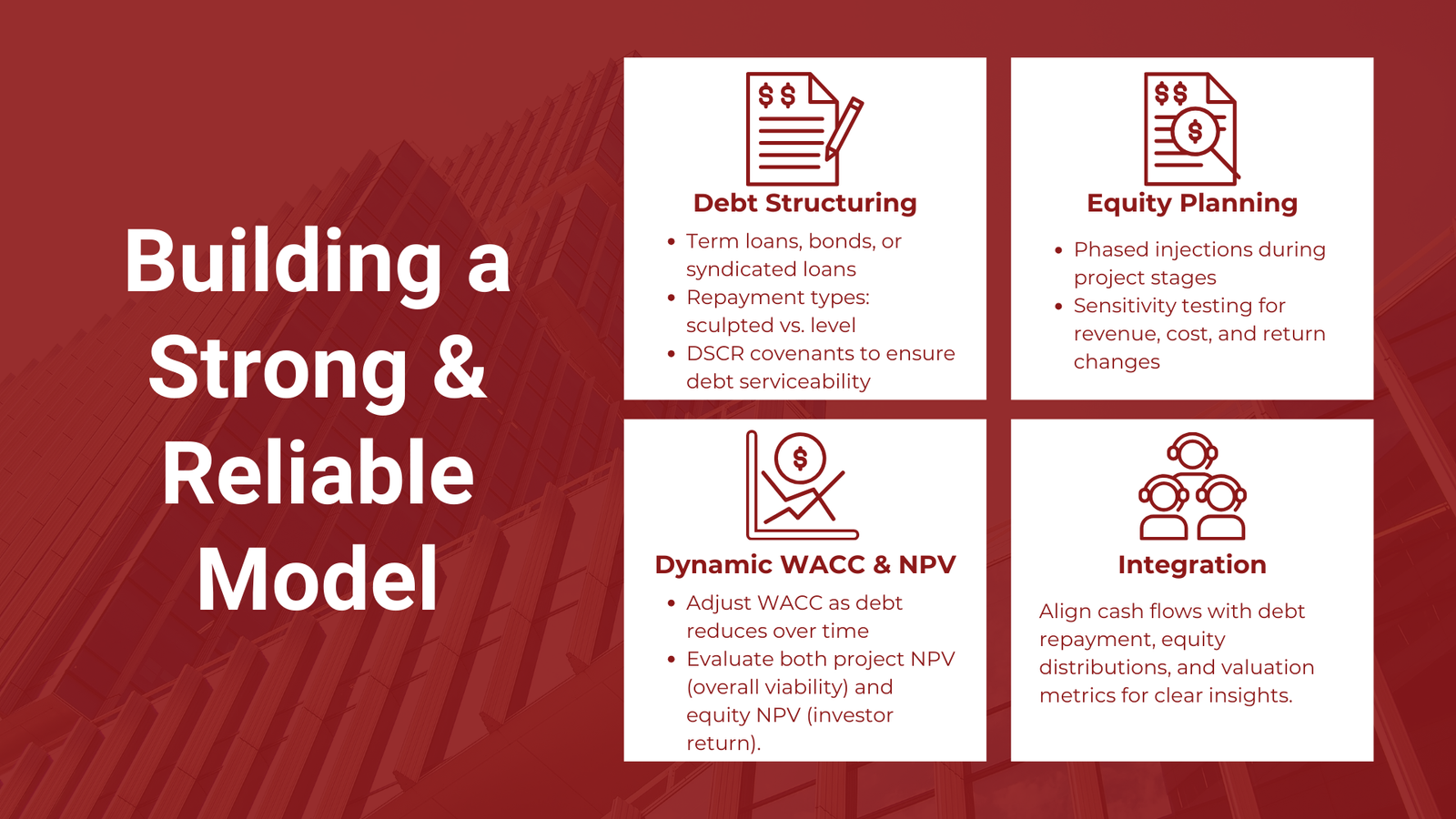

When organizing a debt structure in a project finance framework, the analyst has to specify the debt instrument (term loans or bonds or syndicated loans), repayment term and interest rates as well as a specification whether there will be any grace periods. Covenants are also vital such as Debt service coverage ratio (DSCR) covenants, as it ensures that a particular project has Cash flows, which are adequate to service a debt. A properly constructed model will use several repayment structures similar to sculpted debt repayment (aligned to cash flow profile) as well as level debt repayment (constant amount at each period of time) so as to test the outcome of alternative assumptions.

SIGNIFICANTLY, the overall cost of financing is affected by interest rates and timing of the drawdowns. A project finance model has to reflect accurately the way that interest expense during construction is added as a cost to the debt balance and that affects both the initial equity position and the long run debt service payments. Risk profile can also significantly change when fixed interest rates are chosen as opposed to floating interest rates and risk profile may change when it is assumed that hedging instruments are used. These concepts are often emphasized in Project finance training online for professionals, where participants learn to build robust financial models that account for debt, equity, and risk management strategies.

Equity in Project Finance Structures

Although debt can constitute the larger part of financing, equity however is crucial as it gives risk protection to the lenders as well as showing the seriousness of the sponsor in the undertaking. The equity investors, who are either project sponsors, institutional investors, or private equity firms, are entitled to greater returns than those of the debt holders since the former have more risk exposure. Such returns are commonly achieved by realization of these returns in the form of dividends, profit sharing or finally, a sale off the project.

In case of equity contributions one should consider the timing of equity injection that on most occasions will be in phases that accord with the phases of the construction and the operations. Permitting, engineering, and development funds might be needed early and starting with equity injections might be required prior to raising a debt financing. Cost overruns at a later stage of construction may also be factored in by timing later equity contributions to that milestone.

A typical measurement of equity returns in a project finance model is the internal rate of return (IRR) and equity net present value (equity NPV). These measures assist in establishing whether the project will pass the minimum returns requirements of the equity investors who in this instance is a crucial determinant that would attract the investors. The model must provide an opportunity to conduct scenarios and sensitivity testing to have an opportunity to reckon what impact changes to project revenues, cost, or financing terms may have in equity returns.

Calculating the Weighted Average Cost of Capital (WACC)

Weighted average cost of capital (WACC) is an essential term in the practice of project finance modelling since it conveys the average returns that the debt and equity investors will want to obtain by allocating capital to the project. It acts as a discount rate in the project whereby the future cash flows of the project are measured in present value. It is seen through WACC which includes tax-adjusted cost of debt and cost of equity weighed according to their rank in the capital structure. For professionals understanding weighted average cost method, WACC serves as a crucial concept that connects capital structure with project valuation.

To compute the WACC in the project finance model, the cost of debt is commonly taken as the interest charged on project debt or bond terms but in consideration of the tax benefit caused by the tax deductibility of interest. The Capital Asset Pricing Model (CAPM) which considers risk free rate, the equity beta of comparable projects and the anticipated market risk premium can be used to estimate the cost of equity.

A company should weigh the debt and equity to determine the weighting in calculating the WACC in a manner reflecting the desired capital position of the project throughout its life. Nevertheless, the capital structure in project finance is not fixed since the debt may be paid down, and the project ends up more equity-based. This implies that WACC might have to be dynamically amended in the model to provide shifting proportions of financing.

WACC helps in equating the returns that would be expected in a project in relation to the cost of capital. A situation where the IRR of the project is higher than the WACC will show that the project has a possibility of creating value, otherwise it will mean that the project might not be economically attractive or could be unduly risky.

Applying Net Present Value (NPV) Analysis

Net present value (NPV) is arguably among the most significant metrics in modeling project finance since it would quantify the difference between the present worth of money coming in and that of cash outgoing, during the lifespan of the project. When NPV is positive it implies that the project is likely to create greater value as compared to cost of capital, whereas the opposite occurs when NPV is negative.

Using project finance terms, NPV may be thus computed, both in terms of the total project (discount rate the WACC) and in terms of the equity (discount rate the cost of equity). The sum of project NPV evaluates the general financial justifiability of the project whereas the equity NPV evaluates the returns that equity owners will be able to get after paying off debtors.

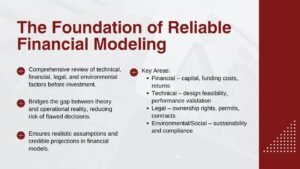

The NPV analysis determines correctly and relies on credible estimations concerning the revenues, cost of running the projects and the costs of capital (capital expenses), costs of financing the project as well as the terminal value (where present). Projects in the infrastructure and energy sectors are often decades-long in term and again even small changes in the discount rates or the assumptions of a long term growth can have a big impact on the NPV result. Sensitivity and scenario analyses would hence be needed to counter check the resilience of the NPV of the project with regards to alterations made in the variable factors.

Integrating Debt, Equity, WACC, and NPV in a Cohesive Model

Whereas individually, each of these elements, that is, debt, equity, WACC, and NPV can be studied separately, the power of a project finance model really comes in the ability to tie them all together logically as a sensible framework uniting financing choices with project economics. Increasing, for instance, the proportion of debt to decrease the WACC because the cost of debt is lower than that of equity, but this will lead to a rise in financial risk and decrease the project resilience to negative revenue results. On the same note, any changes in scheduling equity may affect the capacity of the project in servicing debts and equity IRR.

A proper project finance model will interrelate cash flows being earned by the project used in its operations to the repayment schedule of debt, the distributions of equity and valuation measures. It will also have strong error-checking procedures and civil documentation to allow stakeholders to grasp where the output can be credible.

The Strategic Importance of Structuring

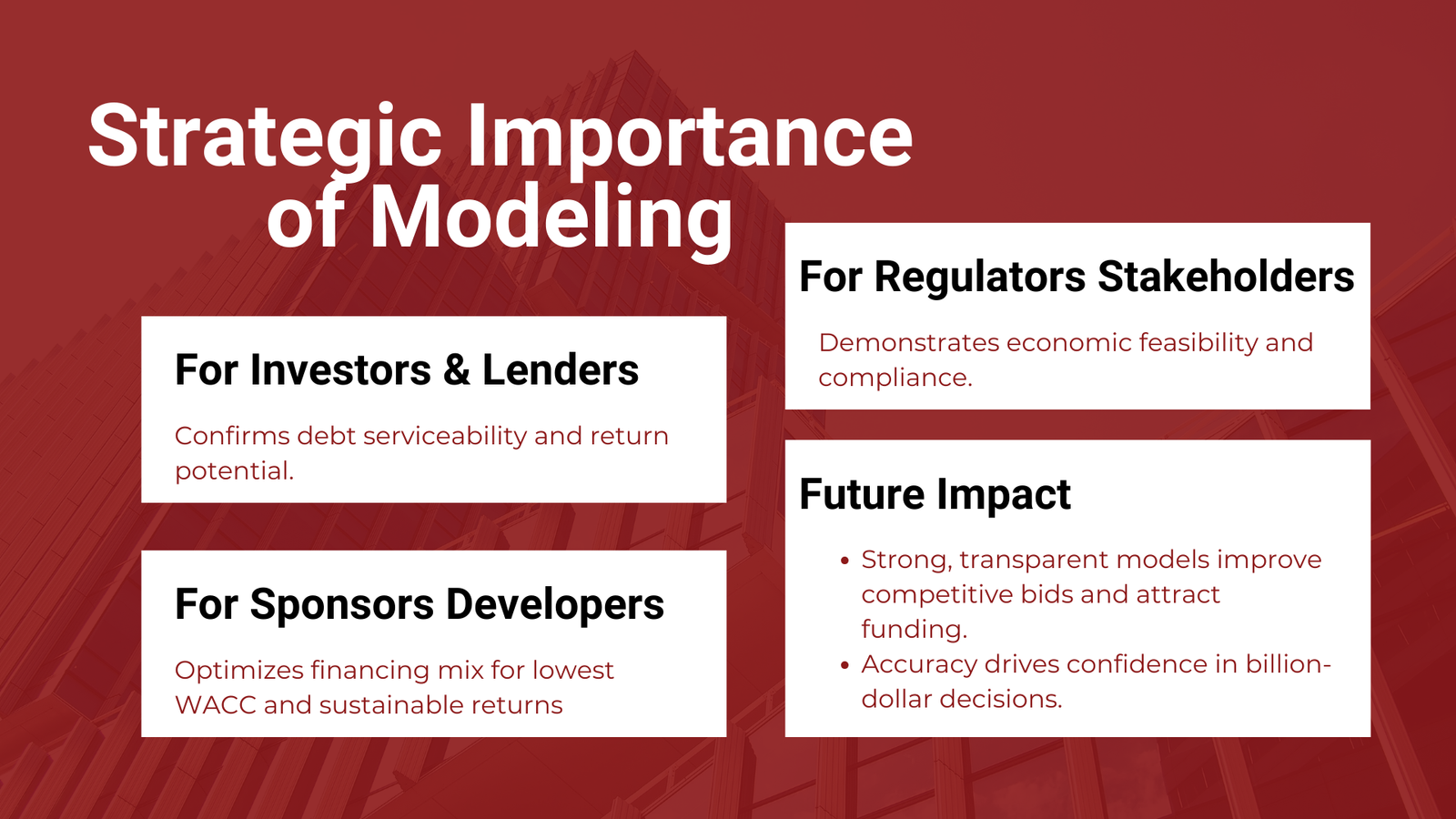

The financial model structuring is not only possible and correct calculations, but also a strategic decision. The very balance between debt and equity, the manner in which the cash flows are distributed among the stakeholders, and the analysis of returns results in the development of a project or its abandonment. Investors will also involve analyzing the model so that it serves as a way of ensuring that loans can be serviced in both realistic and stressed conditions. Equity investors will be concerned with the risks and returns that will be realised and whether it warrants them. Government agencies and other regulators may need to see how the project can be economically feasible on the planned course of its operation.

On competitive bidding, the capability to develop the best financing scheme and to have a highly convincing and clear model could be the determinant of winning or losing a project. Learning the underlying concepts of debt and equity structure, WACC, and NPV therefore becomes a strategic benefit of the developers and sponsors.

Conclusion

Transforming project finance models involves a sophisticated knowledge of the relationship between all sources of funds, cost of capital and value creation. Debt can give the leverage that is necessary to finance large projects whereas equity can give the investors their share in the outcome of the project. WACC is used as a reference to the calculation of yields as pre-determined against total cost of capital and NPV measures the value of the project to be produced, each having a difference in calculation.

Modeling all these elements into one reasonable and responsive financial model would enable professionals to make clear decisions and forecast risks as well as deliver the financial narrative about the project to stakeholders with some reassurance. In any environment with billions of dollars on the line that can be invested once the output of one model is achieved, being accurate about this can not be highlighted enough. Whether you are working in infrastructure development, on energy projects, or any other capital intensive venture, the art of structuring project finance models is a key step in the process of both ensuring project finance success as well as operational success.