How to Model Revenue and Cost Drivers in Finance

Learn How to Model Revenue and Cost Drivers in Finance

A key question in the branch of corporate and investment finance is how revenue, costs and operating drivers interact in a financial model to allow accurate forecasting, valuation and decision-making. Financial modelling is not order plugging some figures in spreadsheets but an attempt to build a logical, organized, dynamic and, hopefully, predictive exposition of how a business performs which can be used to estimate future performance. The various moving parts of a financial model include revenue, costs, and operating drivers as the most important constituents to define profitability, cash flow generation, and eventually, the financial viability of a business.

This paper explains why such elements are crucial, how they are organised in a financial model, and what is important in the practicalities of preparing sound and trustworthy forecasts. It also focuses on the strategic situations that businesses, investors and analysts may face giving a broad approach on why precise modeling of such inputs may result in the difference between a good business choice and an expensive bad choice.

Understanding Revenue in Financial Modeling

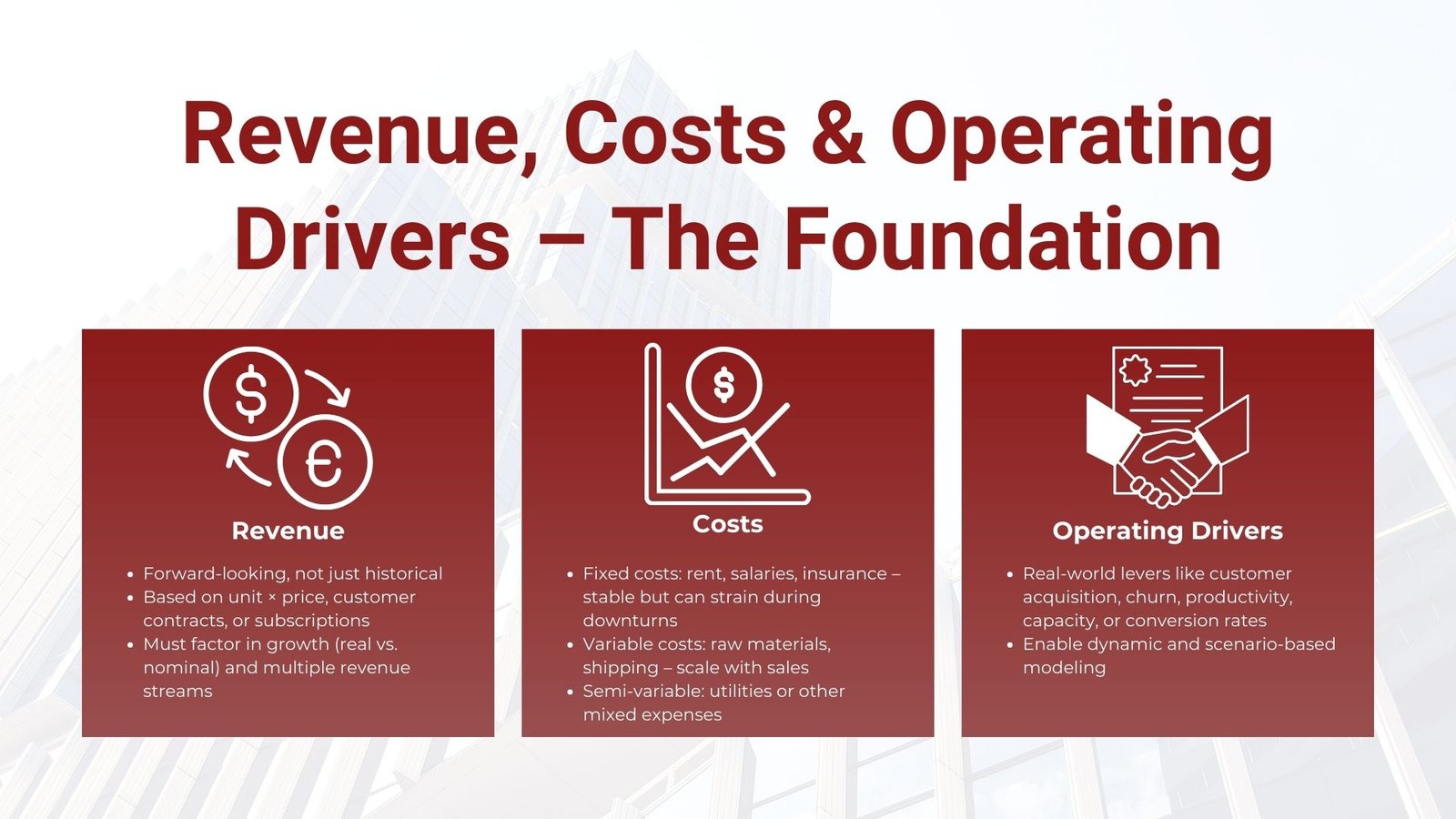

Revenue, also known as the top line, is the beginning of most financial models. It is the overall spending in terms of goods or services sales minus the element of expenses. Nonetheless, when used in the context of financial modeling revenue is more than simply a historic value; a revenue is a forward-looking estimate and could be used to determine the tone of all other calculations in the modeling process.

The revenue modeling varies and it can be of various types depending on the nature of business. In cases of companies based on product, revenue is commonly computed by multiplying the amount of units sold by the average selling price. It can be in terms of customers or contracts, retention rate and cost involved in the recurring purchase per period in case of service based or subscription business. More advanced models can add more than one source of revenue to the base; including a price impetus, seasonal variables, and price presumption.

In the more sophisticated applications of modeling, actual revenue estimates will seldom use one assumption. Rather, they can be associated with various operational lenses including market size, penetration, consumer acquisition, churn and pricing. By using this driver-based mechanism it is possible to better analyse scenarios, in which the model would test how various strategies or market conditions affect the future income of the company.

One of many factors to pay attention to when modeling revenue relates to growth: real growth versus nominal growth. When the effects of inflation are included the resulting figure is nominal growth where the organic or market-driven changes are washed away leaving real growth. This distinction needs to be understood in order to compare forecasts with past performance or industry standards.

Modeling Costs and Their Relationship to Revenue

The second financial modeling pillar is cost. They symbolize the expenses that have to be incurred to earn the revenue and run the commerce. Costs may be classified in a generalized way as fixed costs and variable costs having different behavior under changes in revenue.

Examples of fixed costs include rent, salaries, and insurance which do not change with production or the sale volume. These expenses bring consistency in the operations, but could put a strain on the company in times of reduced income. Variable costs, on their side, vary directly in relation with the output or the volume of sales. Examples are raw materials and shipping costs and commissions.

It is very important to describe the relationship between costs and revenue in a financial model. Variable costs are often presented as a percentage of revenue, called cost-to-sales ratio, so that whatever the revenue changes, costs are easily scaled accordingly. Fixed costs, in their turn, are anticipated to be treated as a fixed amount which might increase in case of capacity augmentation, inflation, or strategic choices.

Semi-variable costs (or costs that both fix and vary) also play a substantial role in businesses that are currently at their growth stages. To illustrate, utility costs can include fixed costs at a baseline rate of charge with a unit per-piece cost tacked on at the end. Cost behavior misrepresentation can result in huge inaccuracy of profitability and cash flow projections.

The comparison of operating expenses (OPEX) and the cost of goods sold (COGS) will also be an important cost factor to consider. COGS are implicitly connected with the goods/services production and influence the estimates of gross margin. OPEX encompasses other overheads, such as marketing, administrative salaries, and R&D which will affect the operating profit but cannot be directly connected with the volume of production. Distinction between the categories is very essential in effective margin analysis.

Operating Drivers and Their Impact on Financial Models

The business activities and measures that drive the growth or changes in the amount of revenue and costs over time are operating drivers. They are the bridge between how well you run the operation and your financial performance. Otherwise stated, they are real world levers that move the numbers within a model.

Typical examples of common operating drivers are the customer acquisition rate, the churn rate, the average order value, the sales conversion rates, the utilization rates, the production capacity and the employee productivity. Driver measures that apply to manufacturing businesses may be the efficiency of the machine, input-output ratio and idling. In the case of retail, accessibility and a maximum number of people passing by a store (foot traffic) and basket size can be critical elements. The retention rate and the lifetime customer value may prevail in subscription-based business.

Incorporation of operating drivers within a financial model increases the foretelling capability of the financial model. A driver-based model is an alternative to using only top-down assumptions such as the assumptions that revenue will increase by 10 percent per annum. As an illustration, instead of expecting that revenue will increase by a certain amount of percentages, the model can estimate the revenue based on the estimated customer base following acquisition, retention and pricing strategy. This will allow evaluating the impact of operational modifications easier, including changes made in the spending on marketing, or an increase in the capacity.

Sensitivity analysis also becomes meaningful should there be operating drivers. In case of a driver-based model, experimentation of minor operational performance alterations can be conducted to apprehend their effect in terms of revenue, costs, and profitability. It is especially valuable in the strategic decision-making, risk analysis and communication to investors.

Interconnectivity Between Revenue, Costs, and Operating Drivers

The strongest financial models acknowledge the interdependence of the process of income, expenses, and operating ratios. These factors are not in isolation. The drivers of revenue are dependent on the level of sales and price, and the cost is determined by both level of operation and efficiency.

As an example, additional production capabilities could allow increased levels of sales that increase revenue. It can however raise fixed costs in terms of extra personnel, facility cost or depreciation. On the same note, any increase in the level of efficiency of production may decrease variable costs, and hence margins when the revenue is held constant.

Analysis of these interconnections enables an analyst and decision-makers to make more feasible and flexible projections. It also allows them to prioritize where they focus their operating leverage, i.e., which places provide small changes in operating drivers with the largest effect on profitability and the cash flow.

Common Challenges in Modeling These Components

Although the reasoning behind using revenue, costs, and drivers of operations may be fairly easy to understand, implementation can be onerous. The temptation to overcomplicate is another typical trap, where one introduces too many drivers or assumptions and does not have enough data to justify their use. This might complicate and compromise reliability of the model.

The other challenge is data quality. Past data is imperfect, sporadic or inaccurate with anomalous incidents that are not the norm like a single sale or an industrial crisis. Reliable projections can best be generated through a judicious normalization of past results and after taking into account many extraneous factors of the business environment like economy, industrial phenomenons, and regulatory aspects.

Another hazard is an assumption bias. Assumptions can occur through the unconscious selection of assumptions that analysts prefer due to a desire, hence make excessively optimistic or pessimistic predictions. This risk can be dealt with by using objective standards, industry averages and sensitivity testing.

Strategic Importance of Accurate Modeling

That which is reflected accurately in revenue, costs and operating drivers has far reaching implications in modeling. It gives a roadmap on resource allocation, budgeting, and performance monitoring as far as internal management is concerned. To an investor and a lender, it provides a clear understanding of the earning potential of the business, its or cost structure and scalability.

Strategically, such strong financial models may inform pricing and expansion strategies as well as investments. An example is a company weighing a new product introduction with a driver-based model to project the sensitivities of various profitability to the prices, sales quantities and cost structures.

In addition, proper modeling helps in the management of risk. Through risk sensitivity measures, businesses are able to come up with contingency plans and rank which operational improvements have the greatest impact. These advantages also highlight the project finance modelling training benefits for professionals, as they gain the ability to apply structured frameworks that improve decision-making, risk management, and long-term business sustainability.

Conclusion

Financial modeling is based on revenue, costs, and operating drivers. Combinations of these give a framework of forecasting future performance of a business in a structured, logical way. When used with accurate models, they allow the businesses to predict challenges, view opportunities and make judgments with confidence.

The success factor is how to combine these elements in a manner that is in line with the business reality. Making its forecasts based on operational realities, and ensuring being more flexible through scenario analysis, the financial models not only turn into a means of reporting, but rather into the means of strategic planning and value creation.

The skills to model these elements of business and the world of finance is not just another type of technical skill; it is an edge, in the highly dynamic world of business and finance. The ability to master revenue, cost and operating driver modelling will be needed in an internal decision making, investor presentation, or strategic planning effort, in addition to any person with a serious interest in long-term financial success.