Valuation of Project Finance Deals: Using IRR, NPV, and Payback Metrics

Introduction to Valuation of Project Finance Deals Using IRR NPV and Payback Metrics

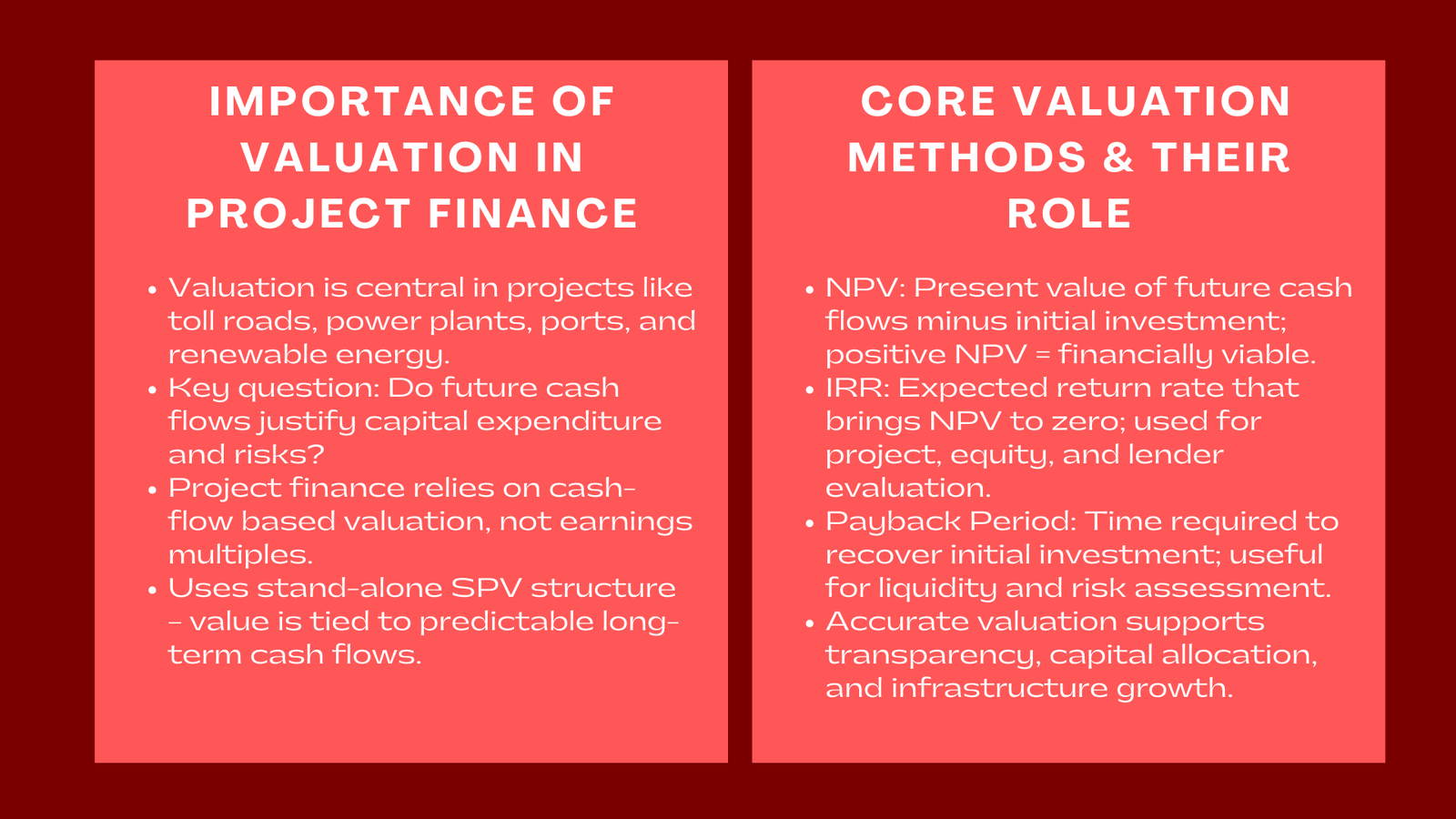

The main part of any project finance transaction is valuation. In the development of a toll road, power plant, port terminal or even renewable energy plant, investors and lenders need to consider the question of whether the cash flows expected in the project will be worth the capital expenditure and project risks. The various stakeholders, long-term debt structure, and regulatory limitations on project finance signal the complexity of the tasks the project finance requires so that proper valuation is a vital condition in decision-making.

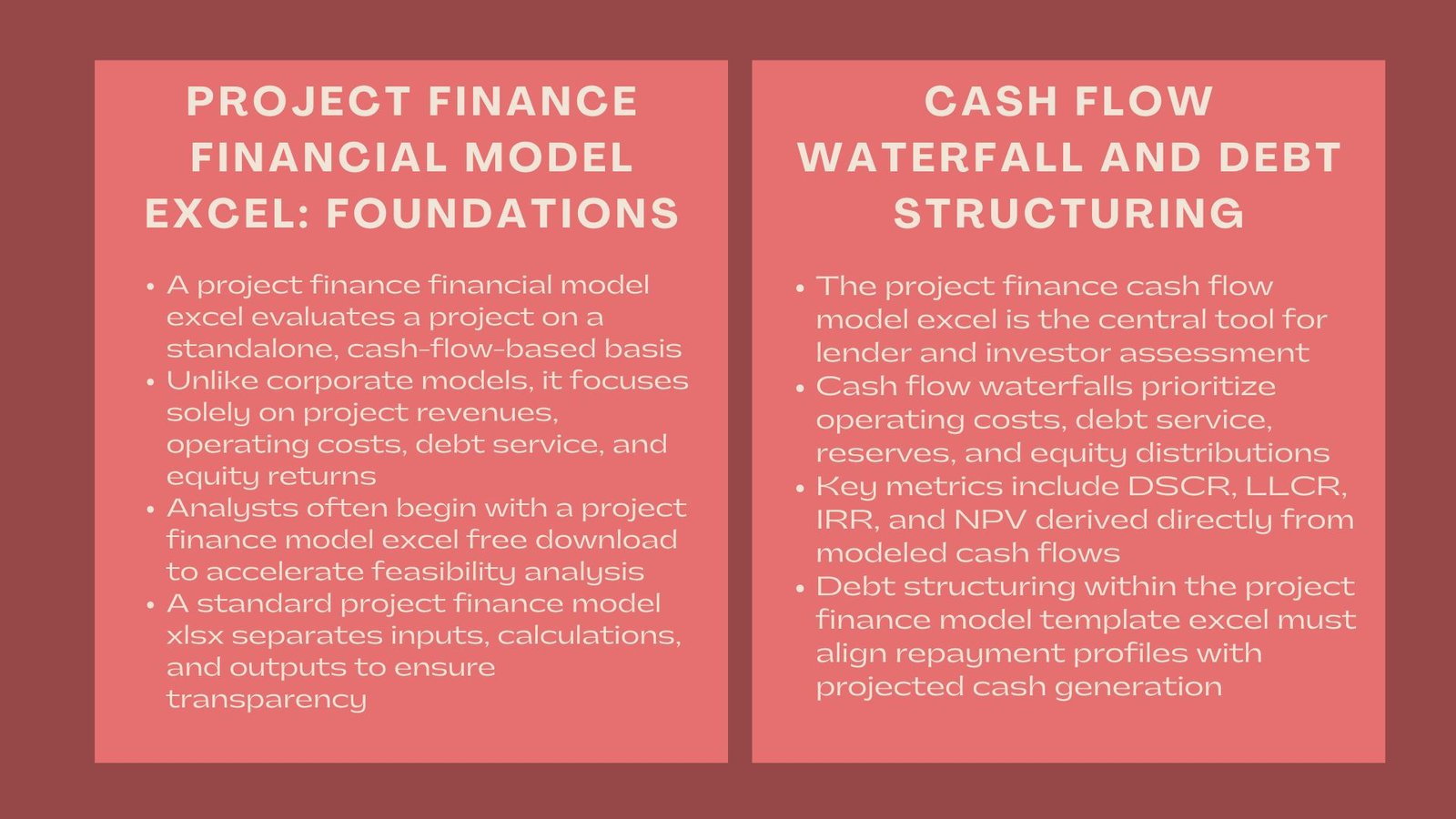

Instead of using valuation of project finance deals using IRR NPV and payback comparability or earnings multiples, as is common in corporate finance, project finance uses the inherent analysis of streams of cash flows in the future. The value of these projects is determined simply by their capacity to produce predictable cash flows over an extended period since these projects are usually designed to be a stand-alone operation or even a special purpose vehicle (SPV). Therefore, the methods of Internal Rate of Return (IRR), Net Present Value (NPV), and Payback Period are the analysis platforms of financial viability.

The paper discusses the IRR, NPV, and Payback analysis methodologies and their use in project finance modelling. It looks into these conceptual bases, their modelling techniques, and their strategic implications to the sponsor lender and policy maker on how to make decisions on investment attractiveness and financial sustainability.

Understanding the Nature of Valuation in Project Finance

Project-Specific Cash Flow Orientation

Financial values of project financing are essentially different to the traditional corporate financing valuation as they separate a project out of the parent company balance sheet. Projects are funded, run, and assessed as independent entities and cash flows are mostly created through long term contracts, user charges or controlled tariffs, which is a core concept often emphasized in a project finance modelling course Singapore valuation module.

Valuation is centred hence not on the enterprise value in market sense, but the ability of the project to service debt, pay dividends and generate acceptable returns of the invested capitals. The capital structure may be very leveraged in most cases and thus the debt-to-equity ratio is above 70:30; therefore the valuation framework should take into consideration the cost of capital and the timing of cash flow to various stakeholders.

The Time Value of Money and Risk Adjusted Returns

All project finance models are based on the fact that the dollar now is worth more than a dollar tomorrow under the principle of the time value of money that acknowledges the fact that an opportunity cost and inflation make the dollar today superior to a dollar tomorrow. The concept will be used to discount cash flows to come up with NPV and returns established through the IRR.

Besides, project finance uses a risk-adjusted model. The valuation rates of discount and the mandatory return are not arbitrary and depend on the risk profile of the project coupled with construction risk, operational volatility, regulatory risk as well as uncertainty regarding demand in the market. The knowledge of these risk drivers will also make sure that the informational results of the valuation are not just numerically acceptable, but economically interesting.

Core Valuation Metrics in Project Finance

Net Present Value (NPV)

The foundation of the project valuation is the Net Present Value. It is the sum of total of the future incomes of cash that are expected to take place in the future and reduced by the first investment. The positive NPV value also means that the discounted cash flows of the project are more than the project cost; hence, the project is financially viable.

In a project financing, NPV estimation includes discounting of post-tax cash flows accredited to the equity investors or in some situations the accumulation of the total project cash flows before funding. The discount rate is normally the weighted average cost of capital (WACC) which consists of the combined cost of debt and equity.

However, in the highly leveraged structures, NPV can be somewhat calculated concerning debt and equity levels. In the perspective of the lender, the concern is on sufficiency of the debt service, and in the perspective of the sponsor, the concern in question is on the cash flows leftover upon completion of all obligations. The specific model therefore identifies the difference between project and equity NPV where it is clear when one considers returns of stakeholders groups.

Internal Rate of Return (IRR)

Internal Rate of Return is defined as the discount rate that the project finance valuation models using IRR and NPV cash flows discount to a zero value. Simply stated, it is an expected rate of the project, including the size and the timing in the cash flow.

Project finance models tend to detach three categories of IRR:

Project IRR is determined by the sum of the future cash flows of the project minus financing which demonstrates the inherent economic efficiency of the project.

The equity IRR, which is the returns the shareholders get after paying its debts.

Lender IRR, which is calculated by taking into consideration the effective yield on debt based on interests payments, charges and repayment terms.

Although IRR is quite an effective indicator, it should be read between the lines. The problem with projects with non-linear or varying cash development can be that they may produce several different IRRs, and overuse of such a client will mislead the decision-makers unless they place the measures into context. Thus, NPV and Payback analysis are usually used as supplements to the IRR analysis in order to have an equal evaluation.

Payback Period

Payback Period is the time in which it takes the cumulative cash flows of the cash investment to be recovered. It does not take the time value of money but it is a good tool for measuring liquidity and risk exposure. Shorter is more comfortable in predicting cash flow of a business and hence will be important in project finance because it will give the investors and lenders a clue that money is likely to be recovered at a young age and also they are not expected to face such uncertainties in the long term.

Single models have a tendency of using the simple and discounted payback period. The latter uses discount factors in order to adjust the cash inflows in the future to a closer level of economic reality. Payback analysis is a complement of IRR and NPV as it shows how the aspect of capital recovery will unfold over time.

Modeling Approach for Valuation Metrics

Cash Flow Construction

Project valuation is based on estimating correct and consistent cash flows, which is done by constructing appropriate and logically consistent statements of cash flow. The model starts with revenue forecasts on the basis of terms of the contract or just a projected demand. Based on this, the operating expenses, maintenance, taxes, and adjustments of working capital are subtracted in order to get the Cash Flow Available for Debt Service (CFADS).

This is followed by subtraction of interest and principal repayments which are used to compute cash flow to equity holders. Equity IRR and NPV are based on these cash flows that follow the financing. When it comes to the reliability of the income statement, balance sheet, as well as cash flow statement it is vital to maintain consistent mediums.

Discount Rate Selection and Sensitivity Testing

One of the most significant judgments which are vital in project valuation is the choice of the discount rate to use. The WACC must be updated based on the structure of financing of the project taking into consideration the cost of debt with tax shields and the required return of equity. Scholars have developed a risk premium to quantify project risks that are hard to predict, e.g., there might be some delays in the timeline of construction or the prices of the commodities used might vary.

With some sensitivity analysis, the users can determine the results of valuation when using varying discount rates, or other operating assumptions. The model shows how well project economics can be supported by experimenting with changes in interest rates, tariffs or the cost of construction.

Scenario and Monte Carlo Analysis

Agreement on project finance Scenario analysis and Monte Carlo analysis can be found in increasingly complex project finance models to test valuation risk. NPV and IRR results during best-case, base-case and worst-case scenarios are used in scenario analysis, when Monte Carlo simulation is used to estimate the probability distribution of values, depending on stochastic input variables. These methods allow investors to estimate probabilistic ideas of risk-adjusted returns and not a unique deterministic value.

Application in Project Finance Practice

Investment Decision-Making

The most important metrics of valuation are the foundation of investment appraisal in project finance. NPV, IRR and Payback are some of the results which are used by the sponsors and lenders to decide bankability, debt pricing as well as capital allocation priorities. Positive project NPV is some indication that this investment is a plus to all parties involved and equity IRR exceeding hurdle rates will show that sponsors have found it appealing.

The outcomes of valuation are directly related to the bidding price as well as the arrangement of the financing proposal in competitive bidding markets. Valuation models that have been sensitised can also be used as a tool of negotiating terms sheets with lenders and investors.

Refinancing and Restructuring Evaluations

The role of valuation is important to the refinance or reorganization situation. The risers in the market conditions lead the project sponsors to revisit NPV and IRR in terms of new interest rates, repayment schedules, or cash flows. The re-calculated metrics can either be used to ascertain the increase of project value because refinancing or restructuring is required to ensure solvency.

In the case of distressed assets, the valuation would assist in negotiating fair conditions between the creditors and the sponsors so that the recovery plans can be viable and fair.

Strategic and Analytical Perspectives

Balancing Short-Term and Long-Term Objectives

Although valuation metrics can be used to provide quantitative clarity, they have to be applied in the context of strategy of the objectives represented by the project. A high IRR might be a good sign of financial efficiency, but it could also represent an overweighted leverage or aggressive assumptions. In contrast, low returns with predictable cash flows could be more enticing to the long-term infrastructure investors.

Striking the right balance between profitability in the short term and sustainability in the long term makes sure that valuation can justify the expectations of the investors as well as social services to the communities, which is important in regulated industries such as energy and transport.

The Role of Transparency and Communication

Results of valuation are usually important in the negotiations among various stakeholders such as lenders, sponsors, regulators and governments. Having credibility and trust is achieved through transparent modelling and documentation of assumptions. Frequent changes in valuation during the project lifecycle enable all the concerned to respond in advance to the changing economic or policy environment.

Institutional and Economic Impact

At institutional level proper valuation of projects leads to efficient capital allocation and Risk management. The financial institutions use the customary valuation techniques to make comparisons of projects in any sector and location. Credible valuation frameworks are also relied upon by the policy makers to evaluate the public-private partnerships (PPP) to make sure that the participation of the private persons results in value-for-money to the taxpayers.

Macroeconomically, properly designed project valuation promotes the development of infrastructures, helps in creation of new jobs and enhances sustainable growth. Valuation fills the gap between society and personal interest due to the connection between financial sustainability and social good.

Conclusion

The financial analysis of projects is focused on valuation. Distinct financial structures are converted into quantifiable values and risks of IRR, NPV and Payback. These tools however, should be used with a sense of discipline, contextualization and high models in order to prevent misinterpretation.

The ability to use valuation techniques variously stands out as an essential characteristic of successful project finance people in a highly competitive and data-driven financing world. Through accurate modeling, clear assumptions and probing foresight, they make all projects sustainable in financial, developmental and long term economic stability.