Airport Investment Finance Modeling

Airport infrastructure finance is the crossroads of government policy, capital investment and business enterprise. Airport finance and modeling is a core skill for infrastructure, project finance and institutional investment finance professionals. Airport investments are not like most corporate finance projects, given the complexity and length of concession periods and regulated revenues, coupled with the capital-intensive nature of construction and complexity of contractual arrangements between governments, operators, lenders and equity sponsors. As a result, airport project finance modeling is one of the most complex – and exciting – areas of infrastructure finance.

Over the last 30 years, airports have been the subject of substantial private investment. From the partial privatisation of Heathrow in the 1980s to the greenfield build-out of Istanbul Airport in the 2010s, billions of dollars of investor and lender capital have flowed into airports across all regions of the world. Each investment has called for a bespoke financial model that can capture the specific attributes of airport revenues, the regulatory framework that oversees aeronautical fees and charges, and the long-term capital expenditure (capex) cycles that define aviation infrastructure. For analysts and associates working in the field, it’s essential to become proficient in these models.

This article highlights the key components of airport investment finance modeling in an accessible manner. It reviews the revenue streams of airports, the typical financing of airports through project financing structures and sources, how to build the model (step by step), and the challenges faced by practitioners. It illustrates concepts with real case studies and provides practical tips for those who wish to build their skills. Whatever your specialism – in infrastructure advisory, project lending, or institutional investment management – this article will help you to get up to speed in project finance training in the airport space.

The Airport Revenue Model: Aeronautical, Commercial, and Regulated Returns

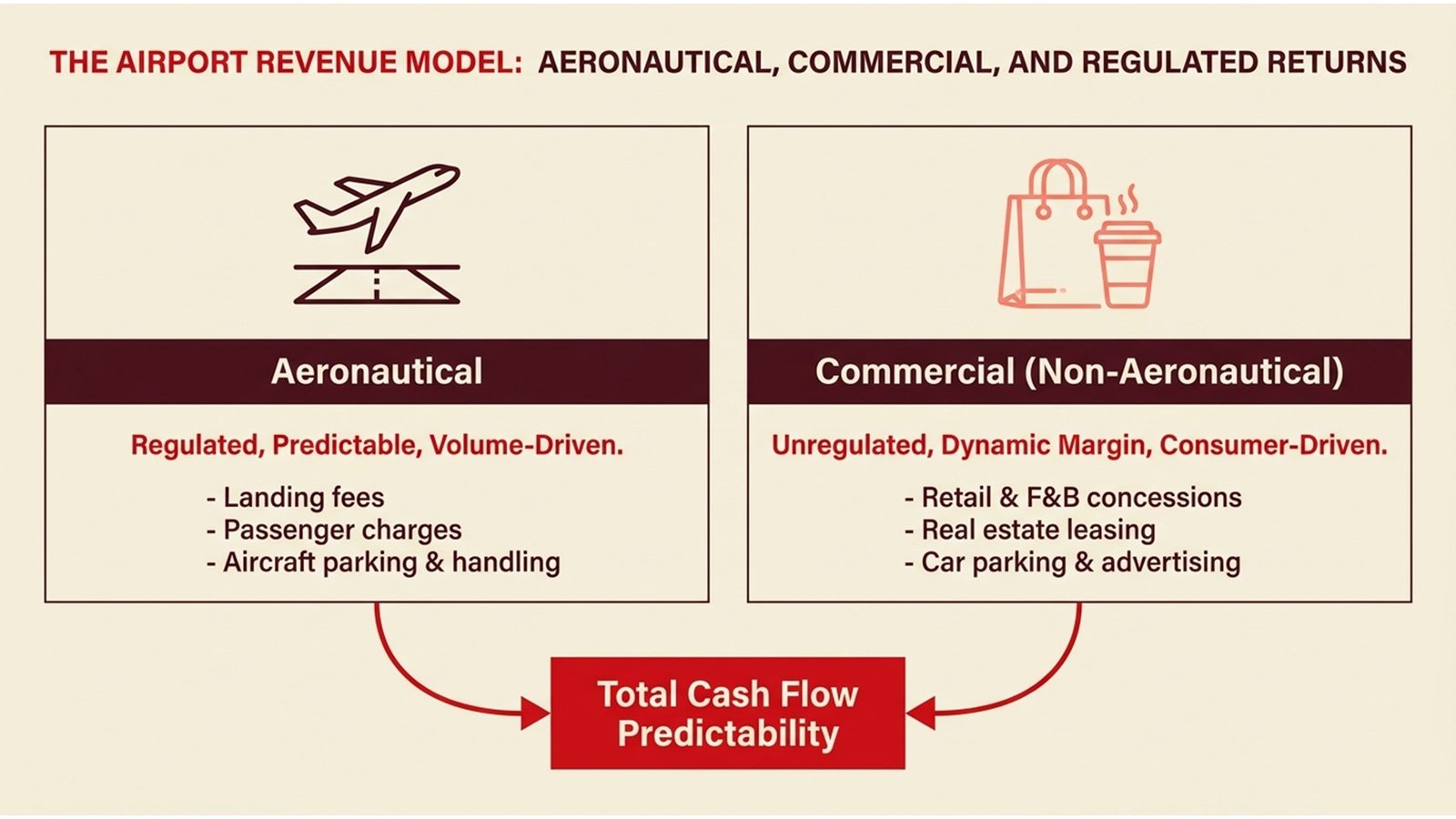

The first step in creating the financial model is for the analyst to recognise the two distinct sources of revenue for airports. Aeronautical revenues, such as landing charges, passenger fees, aircraft parking and ground handling fees, are usually regulated by a government agency or are regulated via price controls in the concession agreement. These are more consistent and volume-based revenues, with a link to passenger and aircraft traffic. Non-aeronautical revenues, on the other hand, are retail and restaurant and hotel concessions, parking, leasing and advertising. These are more commercial in nature, with potentially higher margins and are increasingly contributing to the value of an airport.

The split between regulated and unregulated revenues is extremely important in the financial modeling of airports. Regulated revenues lend certainty to lenders’ cash flow forecasts as the regulatory regime provides a floor for the airport operator’s tariffs (airports can’t charge airlines less than what is allowed) and cost recovery over the regulatory cycle. But the regulatory review period – which is usually five years in most jurisdictions – creates uncertainty about what revenue will be in the future. Unregulated revenues, on the other hand, are subject to the factors of consumer demand, retail mix and management’s ability to enhance the commercial operation. Any model must separate these two streams and consider different growth rates, risk profiles and sensitivities.

This was the case with Fraport, the owner of the Frankfurt Airport. Fraport’s global concessions (at airports in Lima, Antalya, and Ljubljana, to name a few) have distinct revenue streams, depending on the regulatory environment and level of commercial development. In Lima, for instance, the Jorge Chávez International Airport expansion project called for a model that incorporated the effect of a complicated start-up phase, the period of construction with negative free cash flow, and the tariff structure that is regulated by the Peruvian government. For analysts engaged in such deals, the capacity to model these relationships in a clear and transparent manner is a key component to providing best-in-class advice, rather than generic analysis of infrastructure projects.

Project Financing Structures and Funding Sources in Airport Transactions

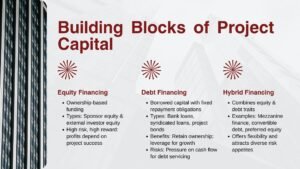

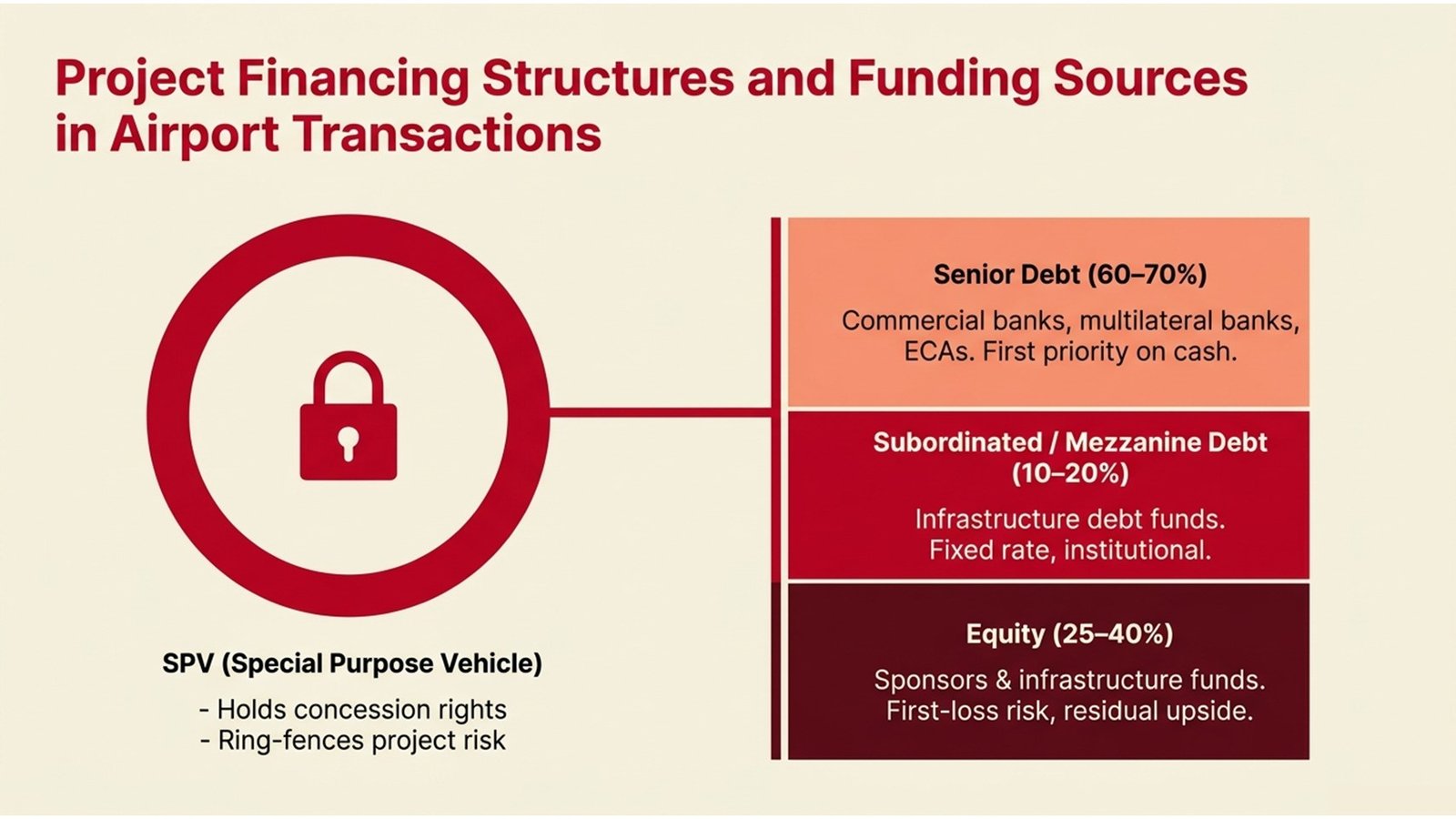

Airport investments are typically financed through project finance structures rather than corporate balance sheet funding. Airport transactions are typically funded via a project finance approach as opposed to corporate balance sheet funding. This is the key element to understanding project financing structures and funding sources, and involves the establishment of a special purpose vehicle (SPV) which holds the concession, uses the assets and raises debt secured by future cash flows rather than by the assets of a sponsor. The SPV structure enables sponsors to isolate project risks, allows lenders to price the debt based on the specific risks associated with the concession and offers a legal structure to manage cash flows and covenants.

The capital structure of a typical airport project includes senior debt, mezzanine (or subordinated) debt and equity. Senior debt – typically supplied by commercial banks, development finance institutions or export credit agencies – is the largest part of the debt structure, and can account for sixty to seventy percent of the project cost. Multilateral development banks like the International Finance Corporation (IFC) or European Bank for Reconstruction and Development (EBRD) are important players in the emerging market airport sector, as both lenders and a “leader” to mobilise private sector lenders. Equity is provided by the concession sponsor (often an airport operator, infrastructure fund or strategic investor) and, as the first loss risk provider, receives the residual cash flows and value appreciation over the life of the concession.

Beyond the basic debt-equity mix, project financing structures and funding sources for airports increasingly involve capital market instruments. Airport revenue bonds, as part of the US municipal bond market, enable airports to issue long-term, fixed-rate bonds at attractive spreads. Debt funds and institutional investors (pension funds, insurance companies) have also emerged as a source of funds for airport projects, given the long duration and inflation-indexed nature of the cash flow, which matches the liabilities of these investors. For the financial modeler, each of these debt instruments has its own set of terms (maturity, interest rate, amortization, and covenants) that need to be modeled correctly to ensure correct debt service and cash flow waterfall.

Table 1: Common Funding Sources in Airport Project Finance

| Funding Source | Typical Share | Instrument Type | Key Characteristic |

| Commercial Banks (Club / Syndicated) | 30–45% | Senior Secured Loan | Variable rate, 10-18 years, comprehensive covenants |

| Development Finance Institutions | 10–20% | Senior / Mezzanine Loan | Below-market rate; ESG conditions; catalytic role for the private lenders |

| Export Credit Agencies | 5–15% | Guaranteed Loan | Financing for equipment; tenor (up to 20 years) |

| Infrastructure Debt Funds | 10–20% | Senior / Sub Debt | Fixed rate; institutional; good for refinancing |

| Airport Revenue Bonds (US) | Up to 50% | Public Bond | Exempt from tax in the US; long maturity; needs to be rated Investment Grade |

| Equity (Sponsor / Fund) | 25–40% | Ordinary / Preference Shares | Subordinated; residual return; IRR-based return expectation |

The Five-Step Process for Building an Airport Project Finance Model

The best practice for developing an airport project finance model is to develop it in a structured manner. Time and time again, when steps are skipped or merged, the result is an internally inconsistent or confusing model for use in negotiation. The five-step process below is the industry standard, and can be followed by the most experienced as well as the most junior analysts.

Process Flow 1: Five-Step Airport Project Finance Modeling Framework

| Step | Action | Key Output |

| Step 1 Traffic & Revenue | Project passenger load factors, flights and passenger yield for both aeronautical and non-aeronautical revenue streams. Use of regulatory tariff assumptions and retail concession rates. | Timeframe of revenue by stream (aero / non-aero) over the life of the concession |

| Step 2 Cost & Capex | Capture staff, utilities, maintenance and concession fees and the complete capital expenditure program (including the different phases of the construction, lifecycle capex and terminal expansion). | Yearly schedule of operating costs & capex, depreciation and asset register |

| Step 3 Debt Structuring | Determine the debt size based on the project cash flows, target leverage ratios and lender requirements. Create the debt schedule – drawdown, repayments and interest. | Debt service schedule; debt service coverage ratio (DSCR); loan life coverage ratio (LLCR); cash waterfall |

| Step 4 Integrated Financials | Integrate revenue and cost schedules, capex and debt schedules into the income statement, balance sheet and cash flow. Fully reconcile and integrate the three statements. | Three-statement integrated model with annual and semi-annual time periods |

| Step 5 Scenario & Returns | Analyse base, best case and worst case scenarios. Estimate equity IRR, project IRR and net present value (NPV). Downside test of debt service coverage. | Table of scenario results: investor return; lender credit |

The first step, traffic forecasting, is key. Historically, airport traffic has recovered from events, such as the 2001 terrorist attacks, the 2003 SARS epidemic and the 2008 global financial crisis, but the nature of the recovery has been different for each event. For new airports or significant upgrades, traffic models are generally developed by aviation consultants like InterVISTAS or ICF, and are the base case assumptions for the financial model. The financial modeler’s task is to understand the assumptions underpinning the forecasts (population of the catchment area, airline route plans, competitive capacity at other airports) and to develop revenue forecasts as inputs to the financial model with the required level of conservatism.

The debt structuring in Step 3 is most important for the cash flow waterfall – the order in which cash is paid out to various parties. For example, in a typical airport project finance transaction, cash flow proceeds are used to cover operating expenses, debt service on senior debt obligations, funding of a reserve account, debt service for subordinated debt obligations and distributions to the equity holders. This waterfall must be accurately modeled because it determines when equity investors will get paid, and whether the debt covenants (such as the debt service coverage ratio (DSCR) and loan life coverage ratio (LLCR) will be satisfied each period. If the DSCR is less than the covenant minimum, a cash lock-up occurs and there cannot be distributions to equity, and potentially the lenders’ enforcement rights accelerate.

Challenges in Airport Project Finance Modeling and Lessons from Real Transactions

Airport project finance is a unique modeling exercise in terms of the complexities and long time frames involved. First among these is the risk of traffic. Airline demand is vulnerable to global economic cycles, oil prices, geopolitical risks and airline strategies. This was abundantly clear during the pandemic, when global passenger traffic declined by more than 60% in 2020, causing most airport project finance models to breach their debt service coverage ratios (DSCR) and prompting debt service waivers to be implemented throughout the industry. Pandemic risk was not factored into most base case models and this has led to a re-evaluation of downside risk in airport project finance models.

The second challenge is the risk of cost overruns. Airport projects are capital-intensive and complex engineering projects, which are prone to cost and schedule overruns. The Berlin Brandenburg Airport, which, after nine years of delay and cost overruns – more than doubling the original EUR 2.8 billion budget – opened in October 2020, was an international lesson in construction risk. The takeout for financial modelers is to explicitly model contingency assumptions into the construction cost schedule, to model the cash flow impact of delayed revenue start-up and to ensure the debt structure includes sufficient liquidity facilities to avoid a “technical” default in the event of a cost overrun.

The third risk consideration is regulatory risk. Many jurisdictions have multi-year regulatory regimes governing airport charges that may not align exactly with the efficient cost base of the airport operation, or with the capital investments. The regulatory system for Heathrow Airport in the United Kingdom, administered by the Civil Aviation Authority (CA) has been a subject of contention between the airport, airlines and the regulator, and has seen challenges to the weighted average cost of capital (WACC) that goes into calculating the regulatory asset base (RAB) which, in turn, impacts the tariffs that go into the financial model. For analysts engaged in project finance training within the airport sector, understanding these regulatory models, the way RAB is calculated, capex eligible for inclusion in the base and efficiency incentives in place are vital aspects of client advisory and lender due diligence.

Table 2: Key Credit Metrics and Typical Benchmarks in Airport Project Finance

| Metric | Formula | Typical Lender Minimum | What It Measures |

| Debt Service Coverage Ratio (DSCR) | CFADS ÷ Debt Service | 1.20x – 1.35x | Operating cash flow’s ability to cover debt service in each period |

| Loan Life Coverage Ratio (LLCR) | NPV of CFADS ÷ Outstanding Debt | 1.30x – 1.50x | The project’s ability to pay back debt over time |

| Project IRR | IRR on total project cash flows | 8% – 12% (real) | Return on total projected investment (before finance) |

| Equity IRR | IRR of equity cash flows (after debt service) | 12% – 18% (nominal) | Return to equity investors (after debt service) |

| Net debt/EBITDA at financial close | Net Debt ÷ EBITDA | 5x – 8x | Leverage at the beginning of the loan; refinancing risk |

| Minimum Cash Balance | Defined in the loan agreement | 3–6 months opex | Minimum liquidity level for debt lock-up |

Another aspect of the modeling process that is underemphasised in project finance education is inflation. Most of the airport operating costs – especially labour costs and energy – are typically linked to general price inflation, while aeronautical revenues in a regulated environment can be indexed to a different measure (such as RPI in the UK or CPI in other countries) or follow a fixed real price path as set by the regulator. Failure to align the inflation assumptions in the cost and revenue blocks will result in wrong profit projections over a 30-year concession. The development of an inflation model – consistently applied across revenues, costs, capex and debt – is one of the most obvious signs of a technically sophisticated airport financial model.

Process Flow 2: Due Diligence Workflow for Airport Project Finance Lenders

| Phase | Activity | Key Deliverable |

| Phase 1 Initial Screening | Approx 15-20 pages of information memorandum (IM), concession agreement summary (CAS) and sponsor background. Evaluate the market environment and the regulatory environment. | Credit screening memo; go / no-go recommendation to credit committee |

| Phase 2 Traffic & Market Review | Determine or review an independent aviation demand study. Evaluate catchment and airline base; competition. | Traffic base case, sensitivity analysis; comments on consultant’s approach |

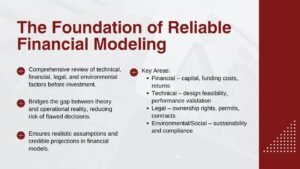

| Phase 3 Technical & Env. Review | Select an independent technical advisor. Review of construction schedule, cost plan, environmental impact statement and operating licence. | Technical advisor report; cost to complete; risk register |

| Phase 4 Financial Model Audit | Appoint a financial model auditor. Validate model, test for circular references, audit cash flow waterfall and stress-test assumptions. | Model audit report; corrected base case; scenario output summary |

| Phase 5 Legal & Structuring | Consider concession agreement, security, lender step-in rights and intercreditor. Term sheet and facility agreement. | List of conditions precedent; signed facility agreement; drawdown plan |

Building Expertise Through Project Finance Training and Practical Application

For those who are interested in building a career at the entry to mid-career level, project finance training for airports involves gaining technical modeling skills, industry knowledge and transactional experience. The technical side starts with the ability to use Excel to build fully integrated three-statement models from scratch, to build dynamic schedules (with multiple tranches) and to build scenarios and sensitivities that automatically update without compromising the internal consistency of the model. These abilities are learnt, not taught, and the best way to develop them is to do model builds from scratch, rather than to modify a template model.

Knowledge of the sector is also critical. Knowledge of the regulatory structures surrounding the setting of airport charges in key markets – the UK CAA’s H7 price cap for Heathrow or Australian Competition and Consumer Commission (ACCC) requirements for Sydney Airport, the concession fees required in Latin American PPP transactions – gives context and allows a technically proficient modeler to become a highly skilled advisor. This skill is developed over time by reading regulatory consultation papers, keeping up with reports of transactions in trade journals such as Infrastructure Journal and Project Finance International and, if possible, gaining experience on transactions.

Perhaps the best project finance education is done by replicating models. Replicating the reported credit metrics of a public information memorandum of a past airport transaction (there are a number available to accompany bond issues or listed infrastructure fund investments) via a financial model requires an understanding of all the model and assumption choices made by the original modelers. The exercise of reconciling the DSCR produced by your model to those reported and understanding why there are differences contributes to the development of the intuitive skills that can’t be taught in formal training. Combined with the discipline of formal courses on airport project finance modeling, provided by specialist training companies, this provides a framework for learning.

Conclusion: Actionable Insights for Finance Professionals

The science and art of airport investment finance modeling requires breadth and depth. The breadth comes from the need to understand the commercial, regulatory and financial aspects of airports, how they are funded through the complex project financing structures and funding sources, and how all these aspects come together into a holistic financial model. The depth comes from the hundreds of hours of model-building, reviewing and stress-testing, and the experience to understand if a number is out of whack, if an assumption is too optimistic and if the model is too complex to be acceptable to lenders.

For those who are early in this career, the first step is to ensure there’s an investment in the skills. Develop three-statement models. Learn how a project finance cash waterfall works. Understand the connections between DSCR, LLCR and IRR on equity, and how each is affected by different variables. These are the tools with which all modeling project finance engagements for airports start and without them, it is impossible to work in project finance advisory, lending or fund management.

Don’t neglect sector knowledge. Read concession agreements. Monitor regulatory decisions at large airports. Follow how the recovery is progressing in various markets in the post-pandemic era, and reflect on the lessons from the pandemic for the assumptions underlying the downside scenarios in pre-2020 models. It is this type of reflection that transforms a good modeler into a good advisor, able to not only create the model but decipher the information in it and explain its importance.

Finally, get some quality project finance training focused on infrastructure and airports. While a solid background in corporate finance is important, it does not build the concession modeling, regulatory, and cash waterfall skills that are required for airport transactions. Through employer-provided training, targeted training providers, or structured self-study using transaction documents, this learning will quickly compound – and in a business where the long-term and establishing technical credibility is essential to success, such training will serve a career well.