Toll Road Project Finance Modeling

Infrastructure finance is a highly specialised and challenging (but also highly rewarding) sector. Toll roads are among the most important infrastructure assets – they are long-lived, large and important to the economy, and have been financed using project finance structures for many decades and in every region of the world. For those in the finance industry who wish to focus on the sector, a good foundation is to become proficient in modeling the financing of toll roads. The models that are applied here are purposefully complex: they must incorporate traffic assumptions, concession economics, multiple layers of debt and reserve account dynamics over a long time frame.

Project finance is more than just a different type of corporate finance. It is about isolating a single project – in this case, a toll road – in a special purpose vehicle (SPV) in order to convince lenders to look first to the cash flows and assets of the project itself (not the balance sheets of the sponsors) to service debt. This poses a very particular modelling problem: all of the assumptions about traffic growth, price rises, operating expenses, and capital expenditure impact the ability to service the debt, and to provide an acceptable return to the equity investors.

This article is geared to junior to mid-level finance professionals – analysts and associates – who are either “new to the room” in infrastructure or project finance, or want to document the knowledge they have gained from working in the field. It provides an overview of the workings of toll road project finance models, the rationale of the cash flow waterfall in project finance, as well as case studies, process flowcharts and tips. If you are seeking to work at an infrastructure fund, development bank, or commercial bank, the concepts and tools in this article will assist in gaining confidence and understanding.

How Toll Road Finance Differs from Corporate Finance

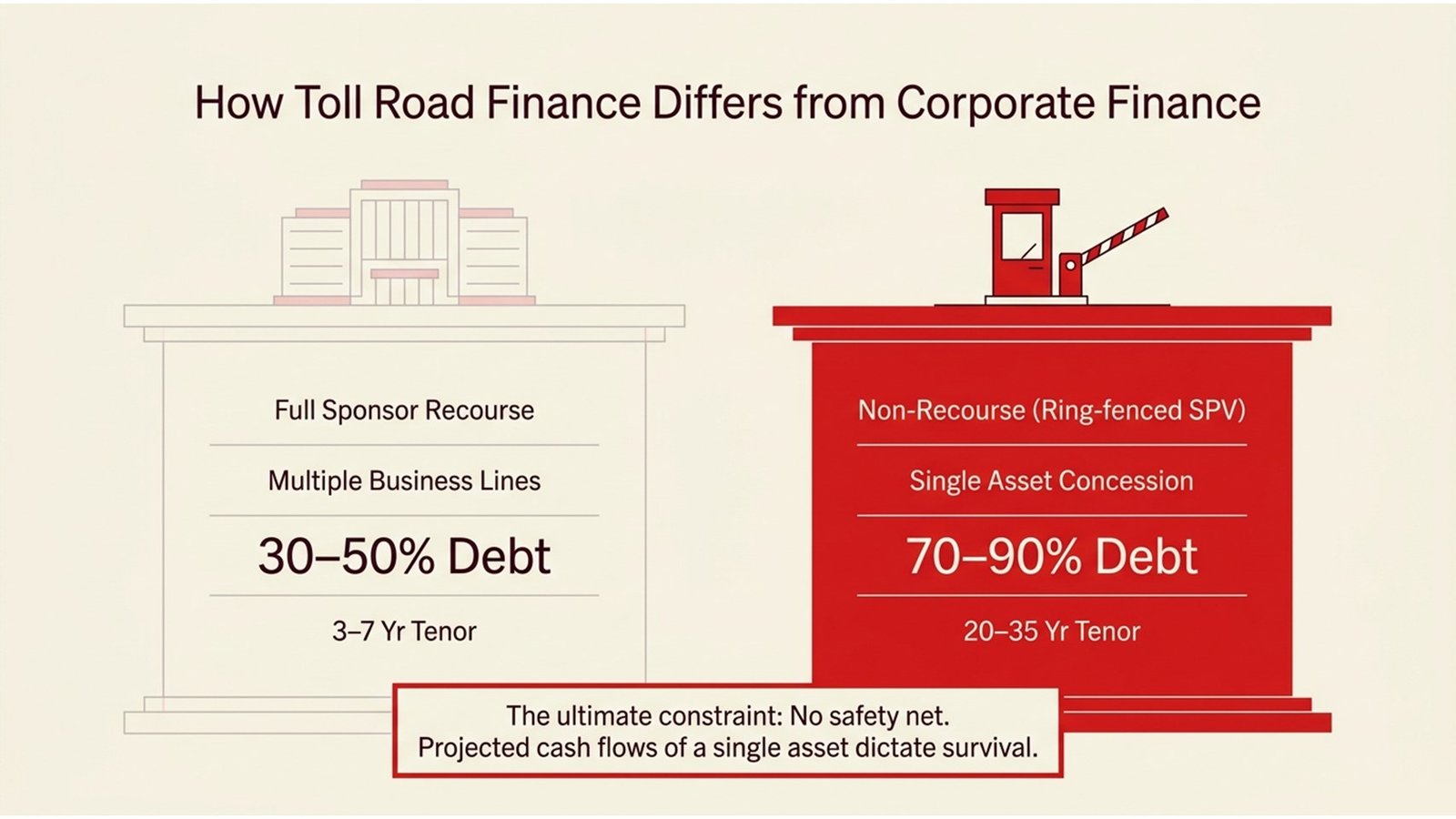

A rookie’s first lesson in toll road project finance modeling is that the method of analysis is different from what is taught in corporate finance classes. In corporate finance, the credit analysis of a company is based on the entire balance sheet, its various sources of revenue and the capabilities of its management across a range of businesses. In project finance, the focus is on one cash-generating asset – the cash flows over the life of a concession agreement – and that’s all that lenders and equity investors look at.

This is both a blessing and a curse. It is a strength as it means that very large infrastructure assets can be financed with very high leverage (70-90% debt) without impacting the sponsoring companies’ balance sheets. It is a constraint because there is no corporate entity to backfill: if the toll road does not perform according to its forecast, then there is no other part of the company to cover the losses. This means that every input to the model is important, and that lenders typically engage in independent traffic and technical audits, and reviews of the model, prior to lending.

Table 1: Infrastructure Project Finance vs. Corporate Finance

| Dimension | Corporate Finance | Project Finance |

| Recourse | Full recourse to the sponsors’ balance sheet | Limited / no recourse to sponsors |

| Security | General corporate assets | Project assets and cash flows only |

| Leverage | Typically, 30–50% debt | Typically 70–90% debt |

| Tenor | 3–7 years typical | 20–35 years common |

| Revenue basis | Multiple business lines | Single asset/concession agreement |

| Key risk metric | Interest coverage, leverage ratios | DSCR, LLCR, PLCR |

The table above illustrates the differences that affect the way a toll road is modelled and analysed. In particular, the project finance debt ratios (Debt Service Coverage Ratio – DSCR, Loan Life Coverage Ratio – LLCR, Project Life Coverage Ratio – PLCR) are all calculated using projected cash flows as opposed to accounting income. Knowing why this is the case and how they are calculated is an essential skill from a good project finance training.

Five Essential Steps in Building a Toll Road Project Finance Model

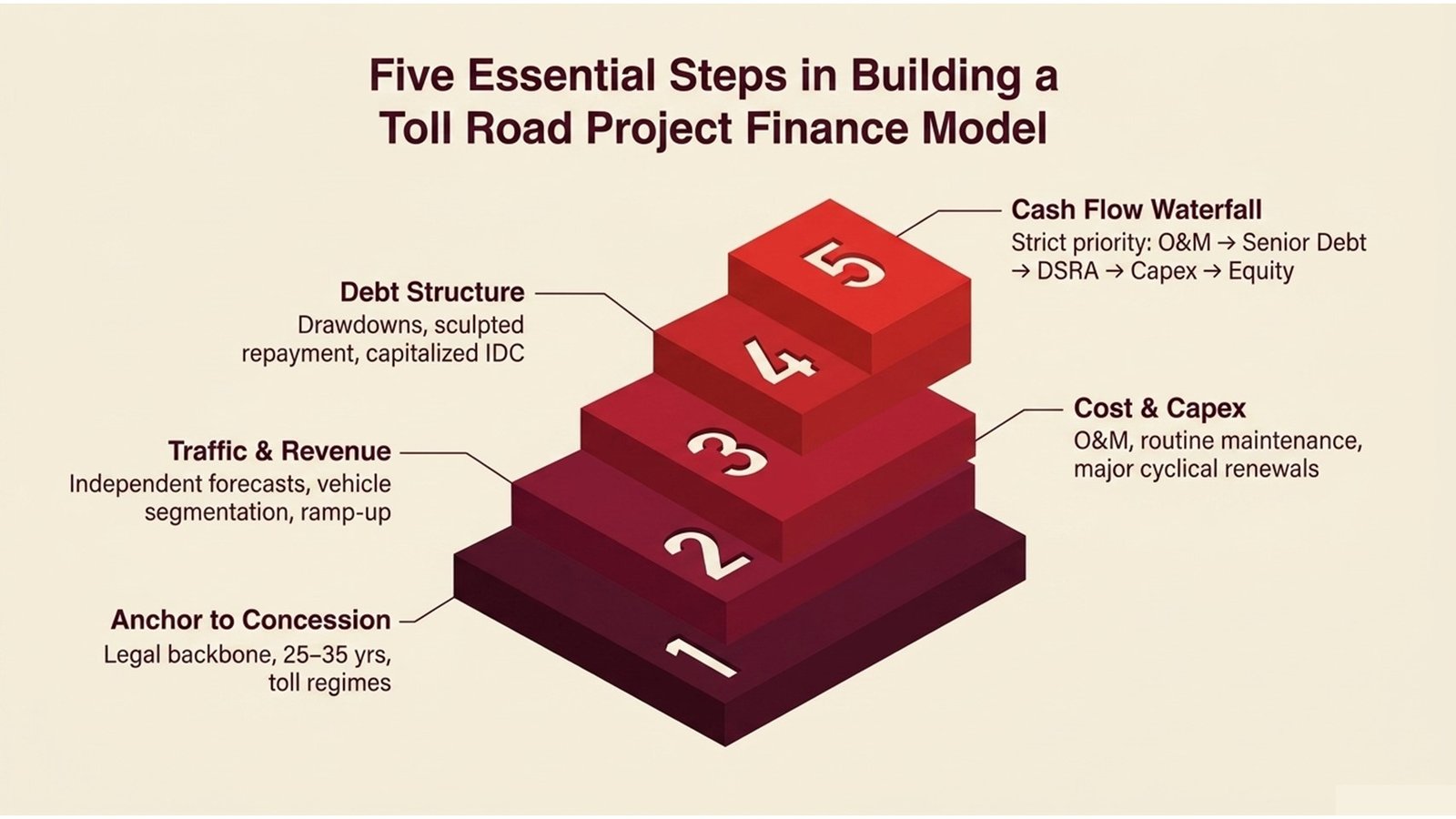

A toll road project finance model is constructed in a series of steps, which build on each other. The most frequent error early career analysts make is to rush through the early steps – or consider them merely as administrative – to get to the output analysis. The approach to model building described in the five steps below mirrors the way experienced analysts work, from scoping to analysis of the results.

Step 1 — Anchor the model to the concession agreement. A concession agreement is the contract that governs a toll road transaction. It sets the length of the concession period (usually 25-35 years) and the rules for setting the toll, as well as the responsibilities of the concessionaire, and events that might end the concession or require compensation payments. It’s the first document that the modeler will read before writing any formulas. All of the commercial conditions – such as toll escalations, traffic guarantees, and lenders’ step-in rights – must be accurately reflected in the model.

Step 2 — Build a traffic and revenue module. Traffic is the main driver of revenues for a toll road. We will often start with a base-case traffic forecast created by an independent traffic engineer that will categorise traffic by vehicle type (cars, light commercial, heavy goods vehicles) and forecast traffic volumes over the life of the concession, based on population and GDP growth, competing route analysis, and trip generation. The modeler will incorporate this forecast into the revenue stream by incorporating the appropriate toll rates and adjusting for build-up assumptions in the initial years of operation, and the concession contract’s provisions for toll escalation (typically tied to CPI increases or a fixed step-up schedule).

Step 3 — Model the cost structure and capital expenditure schedule. The cost structure for a toll road includes toll collection and enforcement, maintenance, insurance, management, and administration (fixed costs), and any other variable costs tied to traffic volumes. Costs should be broken down into the following components: those that increase with inflation, those that are fixed in real terms, and those that increase with traffic. The other part of this is the capital expenditure (capex) budget, which includes the initial construction costs (to be drawn down during the build period) and future major maintenance costs – recurring resurfacing, bridge replacement, technology upgrade – which need to be budgeted and set aside to be financed over the life of the concession.

Step 4 — Construct the debt and financing structure. Typically, a toll road project will have senior secured debt from banks or institutional lenders, but may involve subordinate (or mezzanine) tranches and/or shareholder loans. The model needs to represent each tranche – its drawdown profile, interest rate, and spread (fixed or floating with a swap), amortisation schedule (sculpted to DSCR or straight-line amortisation), and fees. The interest during construction (IDC) must be capitalised and included in the funded cost of the project. The model should test the financing structure under a range of interest rates and traffic assumptions to ensure that it doesn’t become unsustainable.

Step 5 — Integrate the cash flow waterfall and calculate returns. In project finance, the cash flow waterfall is the order of priority in which cash flows from the toll road are distributed to various parties. With the waterfall fully integrated, the model can calculate the various coverage ratios (DSCR, LLCR, PLCR) each period and calculate sponsor returns (IRR and multiple on invested capital) on their investment. These numbers are what the lenders and equity investors will use as the basis for their investment decisions, so they need to be clearly communicated, with all the assumptions made.

Processes, Real-World Applications, and Lessons Learned

It is as important to know how to structure and execute a toll road project finance transaction as it is to know how to develop the model. The transaction is a long process (typically 18 to 36 months from the mandate to financial close) and the model is maintained and updated every time the commercial terms of the transaction are revised or due diligence prompts changes in the model.

Process Flow 1: Toll Road Project Finance — Transaction Lifecycle

| Phase | Key Activities | Primary Participants |

| 1 — Origination | The government releases an RFP / concession; sponsors form a consortium and start a traffic study | SPV owner, equity sponsors, and financial advisors |

| 2 — Structuring | Determine SPV structure, concession, toll, risk allocation and indicative financing plan | Lawyers, financial modelers, and lenders’ advisors |

| 3 — Due Diligence | Independent traffic, technical, environmental and lender model audit | Traffic consultants, independent engineer, lender due diligence team |

| 4 — Financial Close | Signing of loan documents, equity and all project contracts; first drawdown | All lenders, sponsors, the government, and the EPC contractor |

| 5 — Construction | Drawdown of construction facilities; monitoring of construction; cost certification | EPC contractor, independent engineer, agent bank |

| 6 — Operations | Revenue Collection; DSCR testing; reserve account; refinance | O&M Operator, SPV Manager, Lenders, Equity Sponsors |

The transaction process shown above highlights the need not to develop the financial model in a vacuum. The process provides feedback to the model, including the results of the traffic study, adjustments to the cost of construction, lender comments on the debt coverage ratios, etc. A real deal analyst must be able to work with multiple iterations of the model, know which inputs are fixed and which can be changed, and be able to explain the changes to the deal team.

Process Flow 2: Cash Flow Waterfall in Project Finance — Priority of Payments

| Priority | Cash Flow Application | Notes |

| 1st | Operating expenses and taxes – toll collector, maintenance, insurance, management | Paid before any debt service |

| 2nd | Debt service (senior) – interest and principal to senior lenders | DSCR tested at this level |

| 3rd | Debt service reserve account (DSRA) – to top up reserve (6 months debt service) | Lender protection mechanism |

| 4th | Subordinated debt service – mezzanine debt/shareholder loans (if applicable) | Only if the debt service coverage ratios (DSCR) met |

| 5th | Subordinated debt service — mezzanine lenders or shareholder loans, if present | Only if DSCR covenants are satisfied |

| 6th | Equity returns – dividends or return of capital to investors | Cash left over from all the above obligations |

The cash flow waterfall in project finance above is a key concept for the new analyst to grasp. The prioritisation of repayments – operating costs, senior debt, top-ups for reserve funds, subordinated obligations and finally distributions to shareholders – is based on the lender’s insistence that his claims must be fully secured before equity holders receive any reward. As long as the model is properly set up, the waterfall is dynamic so that any adjustment to operating cash flow or debt service impacts cash available for distribution. It’s this “waterfall” structure that makes project finance models difficult to build but readily understandable when done properly.

A good example is the US’s Indiana Toll Road, which was sold by the state of Indiana to a private consortium in 2006 for USD 3.8 billion. The initial concession was funded using a highly leveraged project finance structure and the consortium subsequently ran into financial trouble after traffic growth did not materialise as expected after the 2008 global financial crisis. The concessionaire was forced to file for bankruptcy in 2014. This project is often discussed in project finance training as an example of the risks of excessive optimism with regard to traffic growth and inadequate stress-testing in the base case model. The takeaway is simple: a model that is only valid in the best-case scenario is not a good basis for long-term and highly leveraged financing.

By way of contrast, the North-South Expressway in Malaysia, one of the longest toll roads in Southeast Asia, has been operated under a sound concession and traffic guarantees from the Malaysian government have provided a floor to the risk of revenue. The project’s financing and concession structure enabled a level debt service cash flow over a long life and it has been refinanced on several occasions, as the risk profile improved with time. This journey from construction risk to ramp up, to steady-state operations and finally to refinancing at a lower spread is a typical project finance lifecycle that should be well understood by any toll road project finance modeler.

Key Metrics, Challenges, and How to Navigate Them

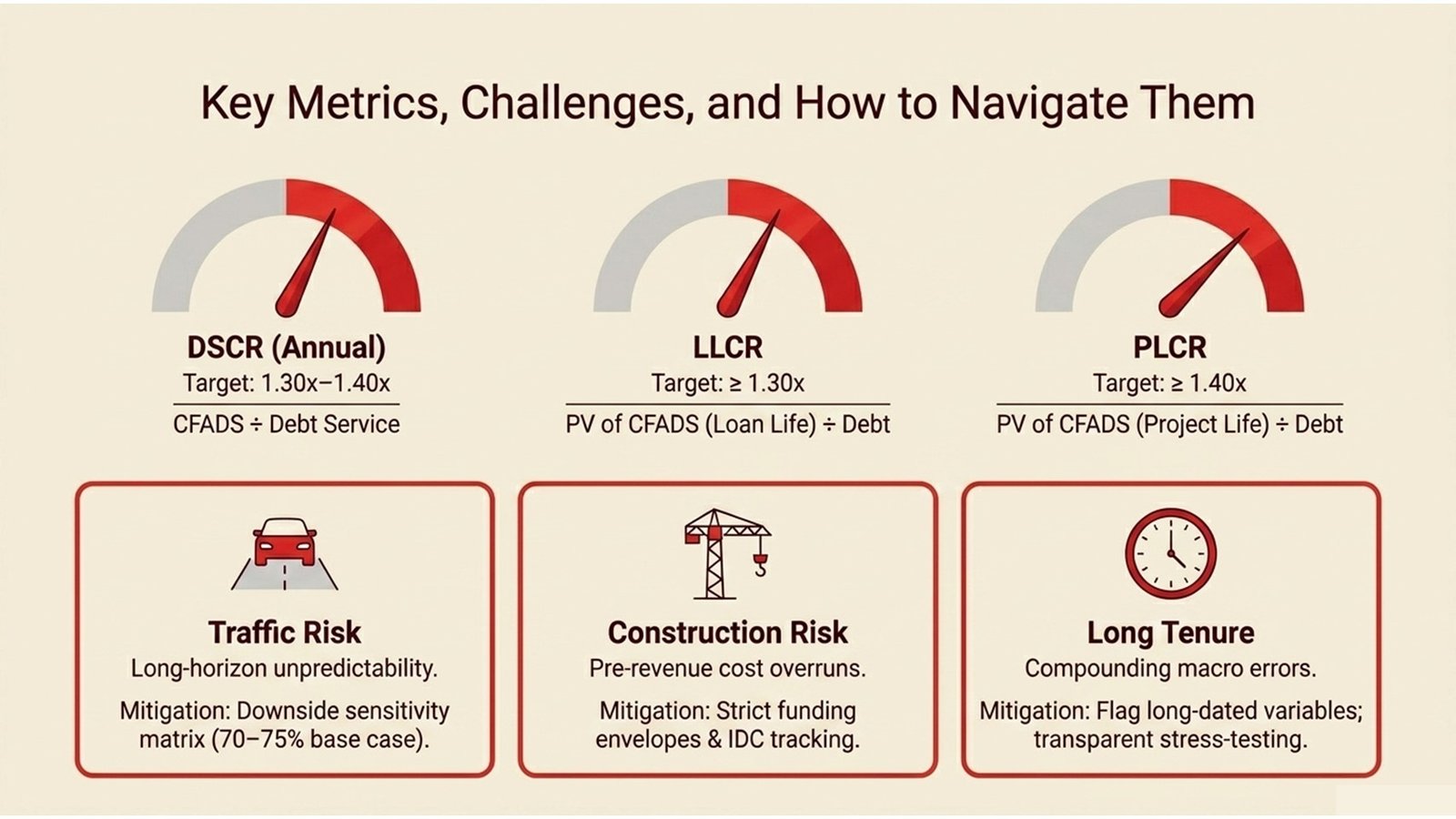

The metrics applied in toll road project finance are tailored to determine whether a project’s cash flows will be sufficient to service debt under various scenarios. Project finance ratios are forward-looking, cash-based metrics, unlike corporate finance metrics such as EBITDA multiples and return on equity (ROE), which are based on accounting earnings that may be distorted by depreciation, amortisation, and other non-cash items. The table below provides a summary of the key metrics that a modeler should know and be able to calculate properly.

Table 2: Key Financial Metrics in Toll Road Project Finance

| Metric | Definition | Typical Threshold |

| DSCR (Annual) | CFADS in a year ÷ debt service in a year | ≥ 1.20x (min), 1.30x–1.40x (target) |

| LLCR | PV of CFADS (5-year loan) ÷ outstanding debt | ≥ 1.30x–1.40x |

| PLCR | PV of CFADS over project life ÷ outstanding debt | ≥ 1.40x–1.60x |

| IRR (Equity) | Discount rate to make equity NPV zero | 10% – 15% market dependent |

| Payback Period | The number of years to recapitalise the equity investment | 8-15 years for greenfield (new) toll roads |

Apart from the complexities of calculating the ratios, the biggest risk in toll road project finance modeling is traffic. Traffic is always uncertain, because it’s dependent on economic growth, competing route options, the price of oil and the way people travel: all of which are hard to forecast over 30 years. The industry’s typical approach is to produce a sensitivity matrix, which demonstrates how DSCR and the equity IRR will vary with changes in traffic ranging from the downside (traffic at 70-75 percent of base case) to the upside. Typically, lenders will require the project to be able to afford the debt even in the downside scenario.

A further issue relates to the construction risk and modeling. During construction, the SPV is committed to draw down debt and equity funding to the EPC contractor, but has no revenues. The model should be able to reflect this – cumulative drawdowns, interest capitalisation in construction and ensuring the cost of the project does not breach the funding envelope (including contingencies). A key source of concern for infrastructure projects is when construction costs overrun and breach the funding envelope – the model should highlight this risk through sensitivities on cost and construction duration.

A third issue is the longevity of the transactions. A project finance modeler today could be projecting costs and revenues to 2055 and beyond. Over this timeframe, assumptions about inflation, interest rates, technology (especially in relation to tolling) and regulations build and build, and are really hard to model. The answer is not to be more certain than is warranted, but to design the model in such a way that the key assumptions that are made in the long-dated future are clearly identified, their sensitivities illustrated and the decision-making team made aware of the uncertainties surrounding the analysis and its outcomes.

Building Skills in Toll Road Project Finance Modeling

The skills required for finance professionals to get into and move up the ladder in infrastructure project finance are challenging but achievable. The expertise needed to build a project finance model – advanced Excel modelling, integration of financial statements, mechanics of the coverage ratio and waterfall construction – can be acquired through training and experience. Project finance training programmes, whether by specialist training providers, professional associations or top universities, should cover the theory of project finance as well as model building. In choosing a training provider, ensure the training approach uses real infrastructure case studies, incorporates sculpted debt financing and explicitly covers the cash flow waterfall in project finance as a separate module.

In addition to formal training, the best way to build skills in modeling the project finance of toll roads is to model recent or live transactions. Many infrastructure funds, development finance institutions and governments release project information memoranda and financial summaries for projects. These can be combined with publicly disclosed concession agreements to provide sufficient information to develop a stripped-down project finance model – a very useful learning exercise. You can check your work against the reported transaction parameters (leverage ratios, target IRRs for equity, concession tenure) to check if your model makes sense.

You also need to gain some understanding of the legal and contractual documents on which the model is based. The concession contract, the lenders’ common terms agreement, the construction contract and the operations and maintenance agreement are all documents that have clauses that impact the model. Finance professionals with this knowledge – not legal expertise, but enough to be able to point out the commercial terms – are much better off than those who view the model solely from a mathematical perspective. It is this level of contextual understanding that elevates the modeller to the advisor.

Conclusion: Actionable Insights for Aspiring Infrastructure Finance Professionals

Toll road project finance is a unique blend of infrastructure policy, long-term capital markets and financial analysis. Models are among the most complex used in finance – capturing traffic economics, construction risk, complex debt structures, and projecting cash flows over a long time frame, all within an auditable model. For young professionals, this skill set provides opportunities to work for infrastructure equity funds, multilateral development banks, commercial lenders and government advisory committees globally.

The first takeaway is to work hard on your core knowledge of the discipline of project finance. Project finance training that involves more than just learning the concepts – how to put together a sculpted debt schedule, how to design a reserve account structure, and how to incorporate the cash flow waterfall in project finance – will pay dividends later. Don’t take for granted the level of technical skill the market demands, even from a junior analyst.

The second thing to keep in mind is to build your models for auditability. Your model will be scrutinised by lenders, sponsors and even auditors on a real deal. A technically flawless, but confusing, model is a curse. Consider the importance of architecture, assumptions and inputs to outputs. The third insight is to consider the risk of traffic. As the Indiana Toll Road and many other cases show, optimistic traffic projections and the leveraged nature of the business lead to weak structures that cannot survive a recession. In your modelling, make sure you test the traffic scenarios and determine the critical traffic level where you are able to meet debt service.

Fourth, get into the practice of reading the concession agreement and project contracts, as well as the model. The model is a quantitative summarisation of the legal and commercial reality – the more you know about this reality, the better your summarisation will be. Fifth, and finally, think of yourself as a translator of both the numbers and the business case when you’re building a toll road project finance model. The purpose of toll roads is to safely and cost-effectively transport people and goods. The better you understand that goal – and the political, economic and social environment in which it’s embedded – the better your work will be valued by your clients.

Infrastructure finance is a long-term endeavour and those who succeed are those who combine the technical skills required with an interest in the assets they invest in. If you can develop that combination, there will be plenty of career opportunities in this field.