Integrating Tax, Depreciation, and Accounting Rules in Project Finance Models

Introduction to Integrating Tax Depreciation and Accounting Rules in Project Finance Models

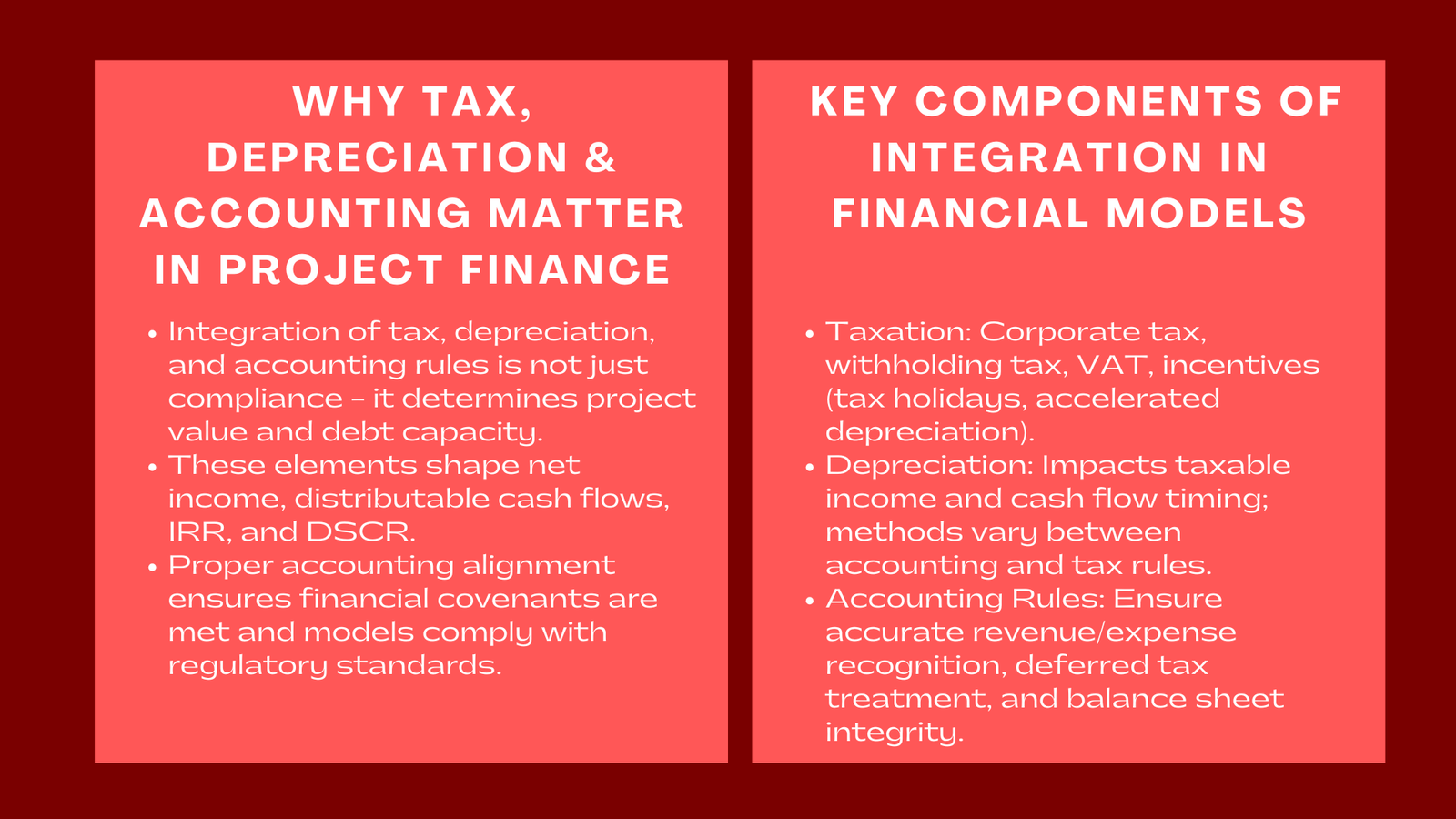

The accounting treatment of projects in the finance of project finance model accounting integration Singapore is not a matter of compliance, but is a determiner of value. There is a significant impact of tax, depreciation and accounting provisions on the profitability of the long term nature of infrastructure and energy projects, cash flow of the companies and the capacity of the company to service its debts. A model that fairly captures these elements gives a real image of the viability of the project whereas a model that does not on or oversimplifies them is at risk of being grossly misrepresentative of the financial results.

When the mechanics of tax, depreciation and accounting are incorporated into a project finance model, financial statistical representations will reflect the truths of the economics as well as legal truths. The relationship between these factors defines the net income, distributable cash flows and basic performance measures like the internal rate of return (IRR) and debt service coverage ratio (DSCR). In addition, accounting acceptance is imperative in meeting financial covenants as well as alignment of the model with regulatory regimes across different jurisdictions.

This paper is an analysis of the integration of taxes, depreciation and accounting regulations in project finance models. It discusses the conceptual foundation of each of the components, the interrelationship between the components, and the ways in which they can be properly modelled in order to guarantee the analytical integrity and reliability of the decisions made.

The Role of Accounting Structures in Project Finance

Accounting as the Financial Backbone

All project finance models have to balance an economic analysis with accounting logic. Though the basis of investment decisions is made on valuation and cash flow projections, the accounting framework would make sure that these projections comply with the set principles of reporting. Accounting structures represent the manner of recognition of revenue and expense, a depreciation of assets, and calculation of taxes, which highlights the project finance modelling Singapore role of accounting in ensuring financial accuracy and compliance.

There are three statements that are usually considered in the financial model and they are income statement, balance sheet, and cash flow statement. The income statement shows profitability in terms of revenues, operating expenses, interest, depreciation as well as taxes. The balance sheet is used to track the assets, liabilities, and the equity positions and the cash flow statement is used to reconcile the changes between the two. When all these statements are combined correctly, the model gives one a complete picture of financial performance not just in terms of cash-based performance but also accounting-based performance that is of great importance to the investors, lenders and regulators.

Bridging Accounting and Cash Flow Perspectives

The emphasis of project finance on cash flows as opposed to accounting profits is one of the hallmarks of the project finance. Non-observation of accounting principles can however cause inconsistencies in the estimation of tax or dividend policy or even the valuation of assets. Depreciation impacts on the amount of taxable income, taxes impact on the amount of distributable cash and accounting regulations dictate the timing of the recognition of revenues and costs.

Making the accounting and cash flow viewpoints meet would make the financial tale of the project appear logical. A balanced model that satisfies the statutory reporting as well as the returns of the investors offers a clear cut bridge that satisfies the analytical requirements of both the financiers and auditors.

Integrating Taxation into Project Finance Models

Understanding Tax Frameworks

A basic part of the project finance is taxation since it directly affects the amount of net cash flows that investors and lenders can receive. The most prevalent ones are corporate income tax, withholding tax and value-added tax (VAT). Tax subsidies may be in the form of investment credits, increased depreciation, tax holidays, or any combination of the above depending on the jurisdiction, can dramatically change the economics of the project.

The first step in the process of modeling taxation is to have an idea about the regulatory framework to be used. The definition of tax base to be used, deductions which can be made and the timing when these deductions should be recognized is given by each country. Thus, the taxation structure under a model has to be flexible and to include the local regulations with exemptions and incentives given to the project under concession agreements.

Modeling Taxable Income

Taxable income usually begins with accounting profit to which such non-deductible or non-taxable items are added. The two most important deductions are depreciation costs and interest costs and the disallowed costs or penalties are to be charged back. The proper order of these adjustments makes the settlement of tax in question to go in line with what the laws have to say.

The financial model has to consider tax loss carry-forwards too -a situation where a loss incurred in the earlier years can set-off the profit in later years and this will cut down the payment of taxes in the future. This needs logical modelling that will trace the accrued losses, use them within the statutory limit and end them when they end up being depleted or time barred.

The correct modelling of taxes helps eliminate overestimation of the amount of the cash flows to be distributed and enables investors to get a true picture of the amount to be given as post-tax distribution.

Cash Flow Timing and Payment

In addition to determining the amount of tax to be paid, timing of the tax payment is also a significant issue. In most states, the tax is paid every quarter or year with possible time lapse between the accrual and payment dates. This time gap generates a balance of depreciation of taxes that need to be reported in the balance sheet of the model.

Inclusion of tax schedule into the cash flow framework is important in that payment amounts will be made at the right times without the cost of affecting the integrity of cash flow available to exercise debt service (CFADS). Such consistency in the accrual and cash-based treatments is a difference between an advanced model and a pure theoretical one.

Modeling Depreciation and Capital Allowances

Depreciation as an Economic and Fiscal Tool

Depreciation is a methodical charge of the capital expenses of items in accordance with the working life. In project finance it is used both to account the cost against revenue, and to achieve fiscal objectives with regards to the amount of deductible expenses and deductible expenses against which a property can be deducted in taxes.

The method used to determine depreciation selected relies on accounting standards as well as tax laws. Although in the case of financial reporting, one can utilize the straight-line method due to the ease, tax authorities might demand accelerated or declining-balance methods to foster investment. The model should adjust these differences with the accountancy and tax schedules depending on the need to use one schedule and another.

Componentization and Asset Classification

Projects tend to be a combination of various types of assets and, therefore, may include civil works, equipment, vehicles, or intangible rights with various depreciation rates. To make refined down to the right depreciation schedule, a refined model will assign the capital expenditure under these categories. The variability in the useful lives and residual value of assets can be considered with the componentization, which allows the use of the different treatment.

This granular model proves essential where a partial replacement of the assets takes place when there are new assets in the process of initiation of depreciation whilst the old ones are also written off. When postponed classification augments the submission of both dollar reports and taxes.

Depreciation and Cash Flow Interaction

Though depreciation is an expense which has no cash effect, it has some impact on cash flows because of the effect it has on the taxable income. Opposite depreciation earlier in life will result in a lower tax in the short term and therefore enhanced current day cash flow although accounting profit will seem lower. An appropriate model can illustrate this trade-off effectively and enable the stakeholders to derive the value of interactions between fiscal policy and accounting treatment in forming financial performance.

Such a relationship between accounting and cash makes sure that the project sponsors can cost-effectively maximize capital structures while ensuring transparency of reporting.

Accounting Rules and Financial Statement Integration

Revenue and Expense Recognition

The accounting regulations apply to recognizing revenues and expenses with reference to time. Where there is a long term contract-power purchase agreement (PPA) or other concession-related projects, recognition of revenues should follow their contractual performance and not the cash receipt. This timing must be captured in this model so that it does not over or understate income.

In the same way, the operating expenses have to be corresponding to the time when they are incurred. Maintenance provisions, insurance and administrative costs are accrued bases although their cash payments are subsequently made at a later date. This makes the income statement reflect a true picture of performance that is going on.

Deferred Tax and Accounting Adjustments

The concept of deferred tax occurs where there are schedule differences between accounting and tax accounting of revenues or expenses. An example is that, accelerated tax depreciation produces short-term tax-accounting profit differences, which cause deferred tax position. On the other hand, in case depreciation in accounting is higher than tax allowances, it is possible to have deferred tax assets.

These timing differences have to be reflected in a professional project finance model which has a reconciliation table on taxable and accounting profits. This is then brought into the balance sheet as deferred tax balances and it is reversed over time as timing differences are made out. Such an integration brings the model to align to the international accounting standards like IFRS and accounting rules for infrastructure projects Singapore or US GAAP and increases its audit worth and financial institutions.

Equity, Retained Earnings, and Dividends

Treatment in accounting also determines the accumulating and declaring of the dividends and as well as the retained earnings. Profit after tax is added into retained earnings and dividends are subtracted on this balance. In case dividend payment is higher than profits made, then equity can be diluted – a move that can break loan security or government regulations.

Simulations of these linkages between income statement and balance sheet would make equity movements to be in line with financial performance and contractual restriction. It also allows the lenders to ensure that only the distributions that are allowed are made as per the agreement of a financing.

Practical Modeling Considerations

Sequencing and Circular References

Applicability of tax, depreciation and accounting as a single model may have circular calculations. Indicatively, interest expense, tax payments have a bearing on taxable income and debt repayment cash respectively. These circularities cannot be carefully handled without iterative methods of calculating or expert settings of excel that assure conservation of models.

Welcomed proper sequencing depreciation as an input in tax computation which separates into profit and cash flow will cause logical inconsistency. Financial logic can be followed easily due to a structured approach to model architecture based on clear documentation being the one that allows the auditors and stakeholders to see the logic.

Jurisdictional Flexibility and Assumption Transparency

The project finance models may be functioning in multiple jurisdictions where tax regimes may be different. The flexibility technique characterized by tax and depreciation modules enables the modeler to compose acceptable change requirements with respect to rules or location of the project. With the help of transparent assumption sheets indicating clearly the tax rates, the method of depreciation and accounting policies, the users can check the congruence with local standards.

Such transparency does not only boost the usability of the model, but also forms a confidence among financiers, regulators and auditors.

Strategic and Analytical Perspectives

Tax Optimization and Value Creation

There would be a lot of value creation of investors when the strategy of integration of tax and depreciation is adopted. Early cash flows are either enhanced with accelerated depreciation, tax credits, or exemption period and, consequently, can enhance project IRR. Nevertheless, highly aggressive tax structuring in the absence of appropriate compliance is a deteriorating threat in the long run. The strategy to balance between optimization and prudence concurs sustainability and integrity in terms of reputation.

On the side of a lender, projection of tax is realistic and confidence on its debt service is enhanced. It will provide creditors with an assurance that the cash generation of the project is healthy based on real statutory requirements, but not suppositions.

Accounting Integrity and Investor Confidence

Professionalism and disciplined governance is a pointer of proper professional accounting treatment. The rating agencies and investors perceive transparent models of accounting as a sign of proper management. On the other hand, earnings, and cash flows would not match as reported which would give cause to raise eyebrows. A model that combines both accounting and accuracy will not be an accounting tool but a tool of institutional reliability.

Institutional and Governance Implications

On an institutional level, tax and accounting can be incorporated into the model of project financial activities to improve the compliance, governance and audit preparedness. On the part of the sponsors, it provides compliance with the agreements on concession and regulations on a national level. To lenders and investors, it gives a guarantee that financial covenants and ratios are calculated using sound data, which is reconciled.

These integrations too are advantageous to public-sector organizations that engage in some sort of public-private partnership (PPP). The proper accounting would create transparency on the fiscal exposures and also on the records made on subsidies or guarantees. Therefore, combating tax and accounting discipline is a field that does not only benefit the individual interests, but also the government.

Conclusion

To incorporate tax, depreciation, and accounting rules into a project finance model is an art and discipline. It needs more than technical modeling skills because it must also be understood in an in-depth way of financial reporting, regulatory frameworks, and fiscal incentives. These factors combined offer the financial story of any project – how the profits will be documented, how the cash flows will occur and how the value will finally be allocated among the stakeholders.

A model which perfectly reflects the interactions becomes not simply an analysis tool, but an overall picture of financial reality. It provides compliance assurance, transparency, as well as the decision-making strength throughout the project life cycle.

Scrutiny, governance and sustainability is the order of the day in a financial environment and this is where the integration of tax, depreciation and accounting regulations are key and can only be mastered. It allows project finance practitioners to reconcile economic analysis with legal accuracy – turn models into the tools of credibility, responsibility and long-term value generation.