Port & Maritime Finance Modeling

Ports are one of the most capital-intensive assets in the world’s infrastructure universe. Before the first ship is moored and the first container is unloaded, several billion dollars have to be invested in a single container terminal in deep water. There are a number of different financial models that underlie such investments, ranging from multiple-decade revenue concessions to complicated construction phases, currency mismatches to regulatory risk, and the long-tail effects of global shipping cycles. Project finance and maritime infrastructure are areas of work in which it is crucial for Junior to Mid-level professionals to enter the port development arena and understand the workings of these models.

Port project finance modeling is an emerging discipline that is a cross-section of capital markets, engineering economics, and infrastructure finance. It’s based on models that will be familiar to anyone who has had experience with debt and equity modeling in other asset classes, such as power plants, toll roads, and airports, but with a maritime twist that sets the demand drivers, regulatory frameworks, and dynamics for a distinctly different type of business. All of these contribute to the models, which ultimately need to meet the requirements of commercial lenders, development finance institutions, and equity investors.

This article gives a systematic overview of port and maritime finance modeling, including a description of port capital structures, the modeling process, real-world issues, and best practices for port governance to keep financial models relevant beyond financial close. These frameworks will provide you with a solid, practical starting point in either preparing for a career in infrastructure advisory, project development or institutional investing. References, too, to the financing of real estate investments are scattered where comparisons of structure with the real estate and property are relevant.

The Capital Structure of Port and Maritime Projects

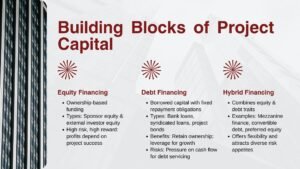

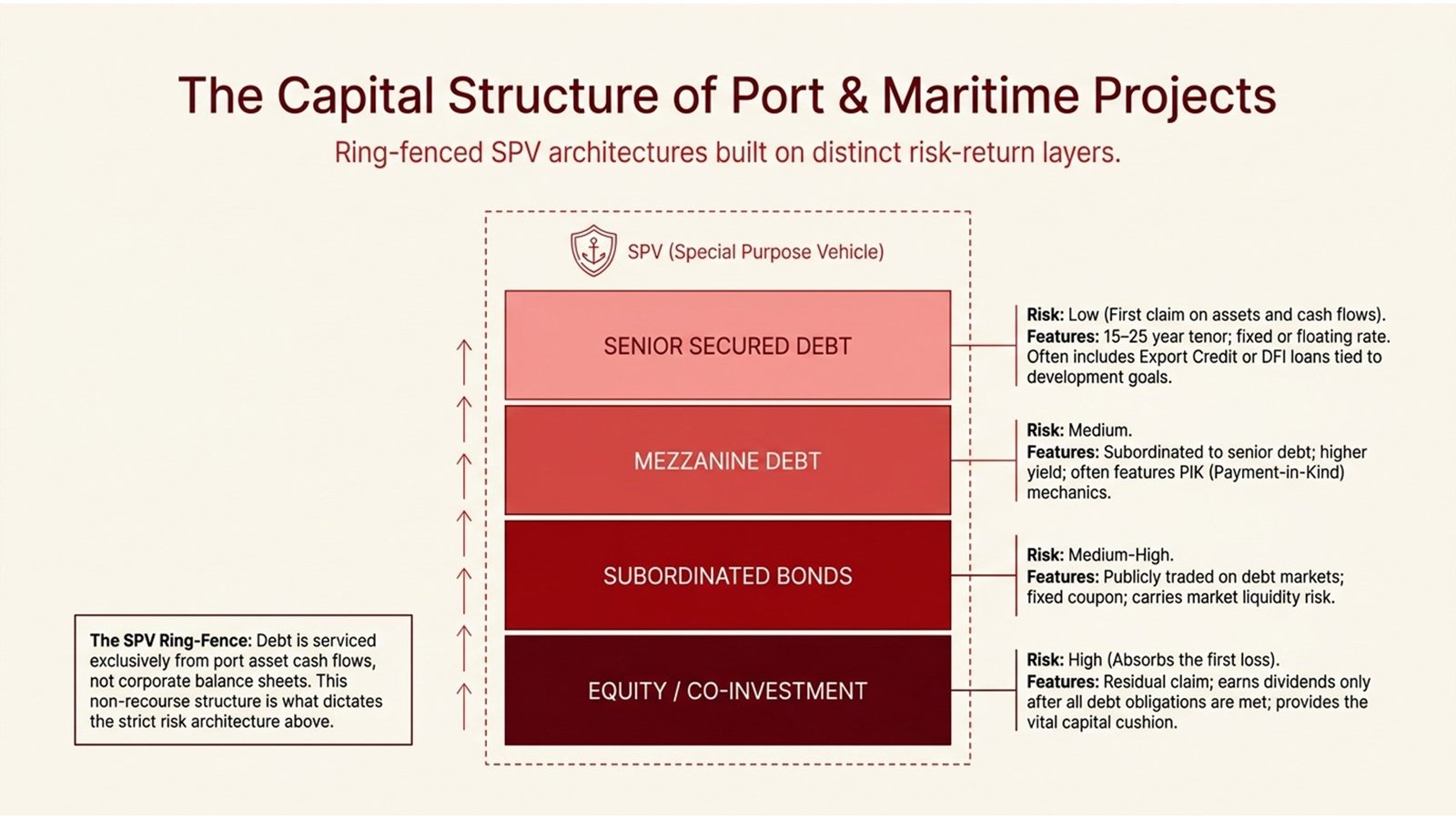

Unlike corporate finance, the balance sheet of the company does not underpin the port project finance; instead, a special purpose vehicle (SPV) is created to finance the port project, and debt is only serviced from the cash flows generated by the port asset. It is this that is the key to project finance’s unique risk architecture, and it is often referred to as non-recourse financing or limited-recourse financing. It’s not a parent company’s creditworthiness that is being relied upon – it’s the creditworthiness of the long-term revenue generation capability of a particular berth, terminal, or port precinct.

Capital structure of a typical port project is a multi-layered structure with each layer of financing having different characteristics in terms of risk, return and seniority. Senior debt, usually from commercial banks, export credit agencies, or multilateral development banks, is at the top of the waterfall of debt, as it is repayment that is based on the conservative cash flow projections of the port. Infrastructure will be funded by the port developer, the infrastructure fund, or the strategic operator and will only start to generate returns once the debt is paid. There are a variety of mezzanine and subordinated instruments between the two that can help sponsors to fine-tune their model of debt and equity and minimize the size of the equity cheque at financial close.

The key to that understanding is that each of the assumptions made in the financial model directly impacts the ability to service the debt and the ability for equity to return the desired rate of return. The main financing instruments employed in port project capital structures, along with their typical risk profile, are outlined below.

Table 1: Capital Structure Instruments in Port Project Finance

| Instrument | Typical Features in Port Finance | Risk Profile |

| Senior Secured Debt | 15–25 yr tenor; fixed or floating rate; first charge on assets | Low — priority claim on cash flows and assets |

| Mezzanine Debt | Higher yield; subordinated to senior; often PIK features | Medium — subordinated but ahead of equity |

| Subordinated Bonds | Publicly traded; fixed coupon; listed on debt markets | Medium-High — market liquidity risk |

| Equity / Co-investment | Residual claim; dividends after debt service; higher return expectation | High — last in waterfall; absorbs first loss |

| Export Credit / DFI Loans | Concessional rates; long tenors; tied to national or development goals | Low-Medium — sovereign or quasi-sovereign backing |

Revenue Drivers and Demand Modeling in Maritime Finance

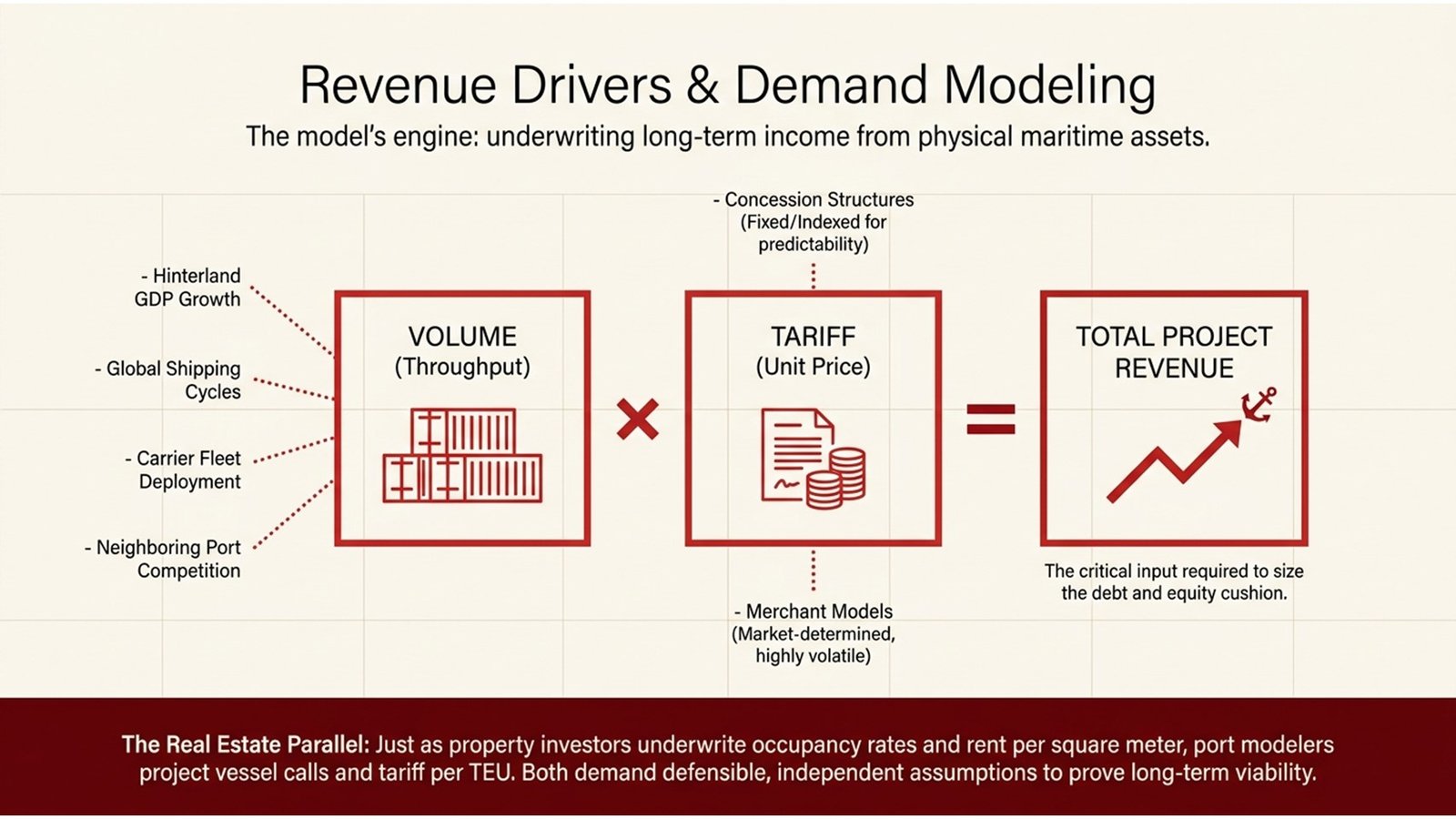

The revenue model is the lifeblood of any port project finance modeling exercise, and it’s where the most time and risk are invested – and that’s where the modelers spend the bulk of their time. There are two key drivers of Port revenues – throughput (number of containers, bulk, liquid or vehicles transiting the Port) and tariff per unit of cargo. Under a concession contract, tariffs can be either fixed or adjusted for inflation during the contract’s term, thus offering some predictability of revenue. Market-determined and highly volatile tariffs are found in merchant port models.

Ports can use a variety of factors, beyond port-related ones, to forecast demand. One key factor is the growth of the hinterland, the geographic area the port serves, and export and import activity is very closely linked to GDP growth. The decision to call at a port, whether it’s one of the big shipping companies or another facility, is affected by global shipping trends, deployment of a ship’s fleet by the shipping companies, and the competition of neighboring ports. Independent traffic studies from specialist maritime consultants are normally prepared by the sponsor for large port projects, which are then stress-tested by lenders’ technical advisors to establish their demand. An equity cushion can be determined by the “downside scenario” provided by the lender and the base case scenario provided by the sponsor.

This is a good analogy to the real estate investment finance industry. A port finance modeler models occupancy, rent per square meter, and lease expiry profiles to estimate net operating income from a project, like a property investor. Both exercises are essentially the same: they seek to secure a long-term income stream from a physical asset, and both depend on how good the underlying demand assumptions are. Whether it’s a logistics center or a Grade A office building, the discipline that is required to build a transparent, auditable, and defensible revenue model is the same.

Five Key Steps in Building a Port Project Finance Model

A port finance model can seem like a daunting exercise with so many variables for those who are constructing or reviewing a port finance model for the first time. The table below outlines the seven-stage flow of the general process used in most professional port project finance modeling exercises, and is followed by a discussion of the five principles that make for good project finance modeling, and which would be rejected by lenders under examination.

Table 3: Process Flow — Building a Port Project Finance Model

| Stage | Key Modeling Activities | Inputs Required | Output / Deliverable |

| 1. Scoping | Define asset type, geography, and tenor | Feasibility study, throughput forecasts | Modeling scope document |

| 2. Revenue Build | Model volume, tariffs, take-or-pay agreements | Traffic studies, concession terms, tariff schedules | Revenue schedule with sensitivities |

| 3. Cost Build | Capex phasing, Opex profiling, depreciation | Engineering estimates, O&M contracts | Capex/Opex model with escalation |

| 4. Debt Sizing | Structure senior debt, size tranches, model DSCR/LLCR | Term sheet, interest rates, amortization profiles | Debt schedule and coverage ratios |

| 5. Equity Returns | Calculate equity IRR, distributions, and payback | Capital structure, distribution policy | Equity waterfall and IRR bridge |

| 6. Sensitivities | Stress test volumes, tariffs, rates, and construction costs | Scenario assumptions from sponsors and banks | Sensitivity matrix and scenario dashboard |

| 7. Audit & Sign-off | Independent model audit, lender review | Completed base case model | Audited model, bankable information memorandum |

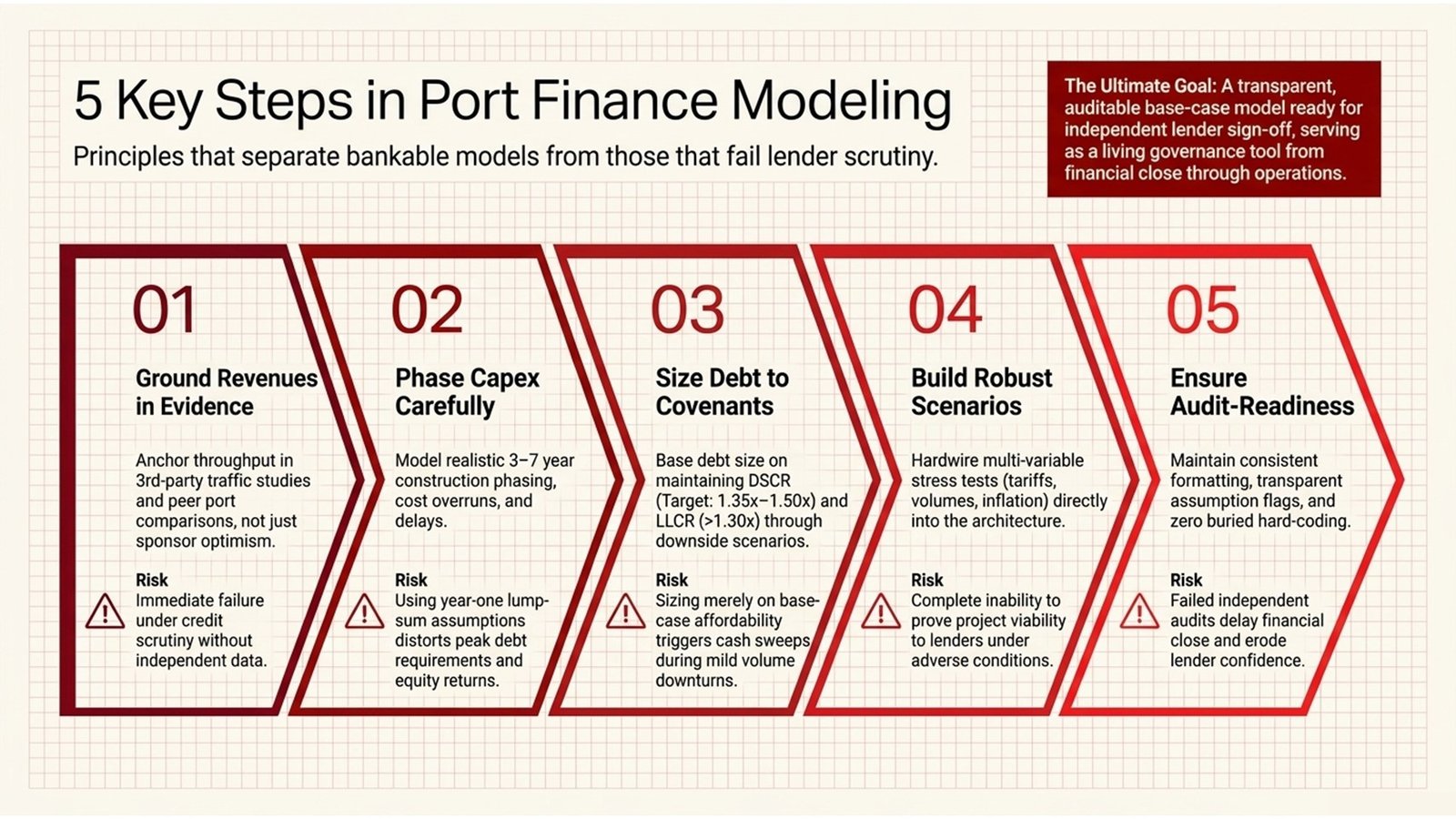

Based on this process, there are five principles that stand out to the professionals creating or assessing port finance models:

- Ground the Revenue Model in Independent Evidence. Make sure that the revenue model is based on independent evidence. One of the most frequently cited challenges to passing the lender review of a port finance model is that the revenue assumptions are inadequate and not backed up by independent information. Unless a sponsor can provide a third-party traffic study, traffic data from similar ports and an explanation of how the port will maintain its market share, his or her rosy-colored forecast of internal throughput will not pass credit muster. The first question to be asked when modeling a port project finance is “What independent evidence backs up each revenue line?”

- Phase the Capex Carefully. The construction of a large port terminal normally takes 3-7 years, and consists of numerous contracts for work, procurement packages and regulatory stages. The financial model should account for realistic construction phases (including cost overrun, delay and scope changes) as the sum of these is directly related to the maximum debt and interest charges on the debt during construction and the returns on the equity investment. The models that take the approach of lumping all of CapEx into year one are not in engineering reality.

- Size Debt Against Covenant Ratios, Not Just Affordability. The actual question in debt and equity modeling with regards to an infrastructure project is not: “how much debt would the project technically be able to service?”, but: “how much debt would the project be able to service for the entire tenor of the loan, even in the worst case scenario?” This is a very significant difference. In a mild volume downside, a project that seems to be well-geared in the base case could experience a DSCR violation, resulting in cash sweeps that would take away the distributions, and potentially even cause the entire capital structure to collapse.

- Build a Robust Sensitivity and Scenario Framework. A good port finance model should always include a well-connected sensitivity analysis to determine how each of the primary value drivers affects the model: the throughput volume, tariff levels, construction cost, operating cost, interest rates, and inflation. In addition to project sensitivity, there is a typical combined downside scenario that lenders are interested in running: a combination of several variables is stressed to determine if the project is still viable in the event of bad, reasonable outcomes. The sensitivity matrix should be derived from the model structure and should not be added on as an afterthought.

- Ensure the Model is Audit-Ready from Day One. No matter how often it is used, the model used in a port project finance is always subjected to an independent model audit by a specialist firm appointed by the lenders. To be audit-ready, everything should be consistently formatted, the assumption flag clearly defined, there should be no “hard” coded numbers, there should be a clear record of what was used, and there should be a logical flow that an experienced auditor can follow without a “tour”. Models that fail the audit are not only embarrassing but also slow down financial close, cause lenders to lose confidence in the model, and can have a significant impact on the terms of financing.

Challenges, Lessons Learned, and Real-World Cases

The history of port project finance is a salutary reminder that large projects have gone wrong, and that – in hindsight at least – such failures were foreseeable from the financial model. When the volume assumptions can be well underwritten and the capital structure has ample headroom, the Port of Baltimore’s Seagirt Marine Terminal, which was purchased by Ports America under a 50-year public-private partnership, is a proven success that highlights the returns that can be achieved for both the public sector and the private operator in a well-structured concession model. The Capex was to be carefully phased, with the main channel deepened to 50 feet and a fourth super-post-Panamax crane added, both being viewed as investments to generate revenue and make a revenue uplift assumption.

The financial problems faced at some greenfield port projects in West Africa and the commodity supercycle of the 2000s, however, show that port project finance modeling based on throughput based on a single commodity corridor may pose risks. Projects that were in the port sector, which had been based on high throughput of bulk cargo into and out of the port, saw the DSCR destroyed when iron ore and coal prices hit rock bottom from 2012. The structural lesson — that commodity-related port revenues cannot be counted on without putting in place take-or-pay contracts with creditworthy counterparties, or that they must be much more heavily financed with equity — is now part of the standard practice in lending guidelines of multilateral development banks.

A comparison with the real estate investment finance is again helpful. The risk of concentrated income will be present where a property developer models a shopping center on assumptions about the number of people who will occupy it, based on one anchor tenant, in the same way that a port developer with income based on a single shipping line or commodity stream is exposed to the same risk. Diversification of revenue sources, multiple terminal operators, multiple cargo types, and multiple shipping alliance calls are not only a commercial goal, but also a financial modeling must-have that directly influences whether or not debt and equity modeling exercises will yield bankable results. In the following table, the key financial considerations that are used by lenders and equity investors to assess the viability of a port project are listed.

Table 2: Key Financial Metrics in Port Project Finance Modeling

| Metric | Definition | Typical Benchmark (Port Projects) |

| DSCR | Net Operating Income / Annual Debt Service | Minimum 1.20x; target 1.35x–1.50x |

| LLCR | PV of future cash flows over the loan life / Outstanding debt | Above 1.30x throughout the loan tenor |

| Equity IRR | Discount rate at which equity NPV equals zero | 12%–18%, depending on market and risk |

| Project IRR | Returns at the unlevered project level before financing | 8%–12% for brownfield; higher for greenfield |

| Payback Period | Years for cumulative cash flows to recover the initial investment | Typically 10–18 years for major port projects |

| Gearing Ratio | Total Debt / Total Capital | 60%–75% debt is common in project finance structures |

The construction risk is another risk that has been a hit or miss with port finance models. It was a reminder of the execution risk of even the most technologically advanced infrastructure projects when the Panama Canal was expanded, despite numerous financial models forecasting its completion, which were only realized in 2016 after many cost overruns and contractual disputes. In port project finance, construction risk is usually covered by using fixed-price engineering procurement and construction (EPC) contracts with performance bonds and a financial model with a contingency reserve and a realistic drawdown schedule that takes into account the risk of delay. Modelers who don’t factor sufficient construction risk buffers into their port project finance modeling are simply hiding the risk from the equity investors.

Governance, Model Lifecycle, and Career Relevance

A port finance model is not a one-off; it continues to serve its function after financial close. The financial model is a living document in well-governed project finance transactions and is constantly updated as actual Capex costs are monitored against the budget during the construction period and during operations, when actual throughput and tariff revenue are monitored against the forecast. As relevant as the build itself is the governance model that dictates ownership of the model, who has the ability to make changes to the assumptions, and how changes are documented, as this part of the project will impact the long-term financial success of the project.

The process flow below outlines the complete process governance framework for a Port Finance Model – from construction to refinancing or asset sale. It is applicable to debt and equity modeling of other infrastructure asset types as well, and anyone who adopts this mindset early in their career will be able to directly apply it to other ports, airports, toll roads, and energy assets.

Table 4: Port Finance Model Governance and Lifecycle Framework

| Phase | Actions | Success Indicator |

| Initial Build | Construct base case; agree on key assumptions with sponsors | Base case approved by the project committee |

| Lender Review | Submit to arranging bank; respond to queries; revise assumptions | Term sheet signed; credit approval granted |

| Financial Close | Freeze model; conduct an independent audit; execute financing docs | Model audit passed; funds drawn |

| Construction Phase | Update actuals vs Capex budget; reforecast completion date | DSCR projections remain above covenant levels |

| Operations Phase | Annual model refresh; compare actual vs forecast volumes | Covenant compliance confirmed; distributions approved |

| Refinancing / Exit | Rebuild the model for the new capital structure or the sale process | Equity IRR confirmed at or above hurdle rate |

The governance framework is especially relevant to junior to mid-level professionals since it sets the context for the use of financial models in the profession. A model for a lender’s credit committee is different from a model for an equity investor’s investment committee, and both are different from the project company’s finance team, who would use the model to check on the compliance of the covenants on a quarterly basis. One fundamental competency in project finance modeling for ports is understanding what version of the model you are modeling and the decisions the model is supposed to be basing.

Port and maritime finance modeling is not only relevant to the port and maritime industry itself, but it also has a wide scope of applicability. The analytical techniques that can be learned using port project finance modeling – cash flow modeling with long time scales, covenant analysis, optimizing capital structure, and sensitivity analysis – can also be applied to real estate investment finance, energy project finance, and infrastructure fund management. In any investment where there is a significant amount of capital involved, a professional who can develop and review a 25-year portfolio finance model, including the debt scheduling, equity waterfall, and the creation of scenarios, is useful. In fact, the lenders’ technical requirements in port transactions are even greater than in most other types of asset transactions — making experience in this area actually a competitive hiring advantage.

Conclusion: Actionable Insights for Aspiring Port Finance Professionals

Port & maritime finance modeling is an art to both the technical and commercial aspects of the job. In the end, the financial model is a decision-making tool; if the project needs to be financed, a financial structure, if it needs to be funded by debt, or a check on whether the project is viable in the event of a demand slowdown, the quality of the decision will depend solely on the quality of the financial model supporting it. For practitioners who are working on developing competencies in this area, there are a few takeaways.

First, spend some time getting to know the demand side before getting started with the financial model. The revenue inputs in any port project finance model are the most critical inputs in the overall model, and those which are most frequently questioned by the lender, the auditors and co-investors. A modeler who can explain not only what the throughput assumptions are but why they can be justified based on the competitive situation, on the economics of the hinterland and on the dynamics of the shipping network will be worth so much more than a modeler who can merely produce a spreadsheet.

Second, master the debt and equity modeling language – DSCRs, LLCRs, equity IRRs, distribution waterfalls, etc. – and know how to interpret intuitively what changes in operating assumptions mean to these metrics. The skill of explaining to a non-technical stakeholder the impact of a 10% decrease in throughput in year three to get the DSCR below the covenant levels and thus trigger a cash sweep is a quality that separates senior analysts from junior analysts, and comes from building enough models to acquire some real insight.

Third, apply the concepts of real estate investment finance where they can be of benefit. Port assets, like property assets, are long-dated physical assets that provide contractual income streams from port tenants or users. The asset valuation techniques, income capitalization, lease structuring, and refinancing analysis, all of which are well developed in real estate, have their parallels in maritime finance, and there are those who live in both worlds who can seamlessly cross between them and thus add to the knowledge and experience base of infrastructure investment firms.

Lastly, make all financial models professional documents, demonstrating your analytical credibility. During a port project finance modeling, models are examined by the lenders’ technical advisors, independent model auditors, and regulators. The model is not only a technical asset, but it’s also a professional statement of the rigor and care with which you approach complex problems, and it’s logically structured, clearly documented, and easy to audit. That’s not a triviality in a sector where billions of dollars of capital allocation are based on the results of financial models. It is the point.