In project finance models, cash flow is forecasted based on clear assumptions about project revenues, operating expenses, financing arrangements, and cash flow timing during the project’s construction and operation/loan repayment periods. Through a process of cash flow analysis in project finance, long-term forecasting, cash flow waterfalls, and risk allocation, revenue drivers are directly connected to debt service and equity returns. It discusses each and every step of revenue forecasting, cost modelling, building waterfalls, and analysing the DSCR to ensure proper financial planning step by step.

What Is Cash Flow Projection in Project Finance Models?

In project finance, cash flow projection involves providing a forecast of all cash inflows and outflows to a project over its economic life, broken down into two stages: the construction phase and the operating phase. The cash flow in each phase varies, and the model should reflect the cash flow accurately.

Typically, construction cash flows are mostly negative (cash outflows) as equity is put in, the debt facility is drawn down, and payments are made to the construction contractors. The project pays out revenues during the operating phase that are required to pay for operating expenses, to pay back service debts, to build reserve accounts, and eventually for returns to equity investors.

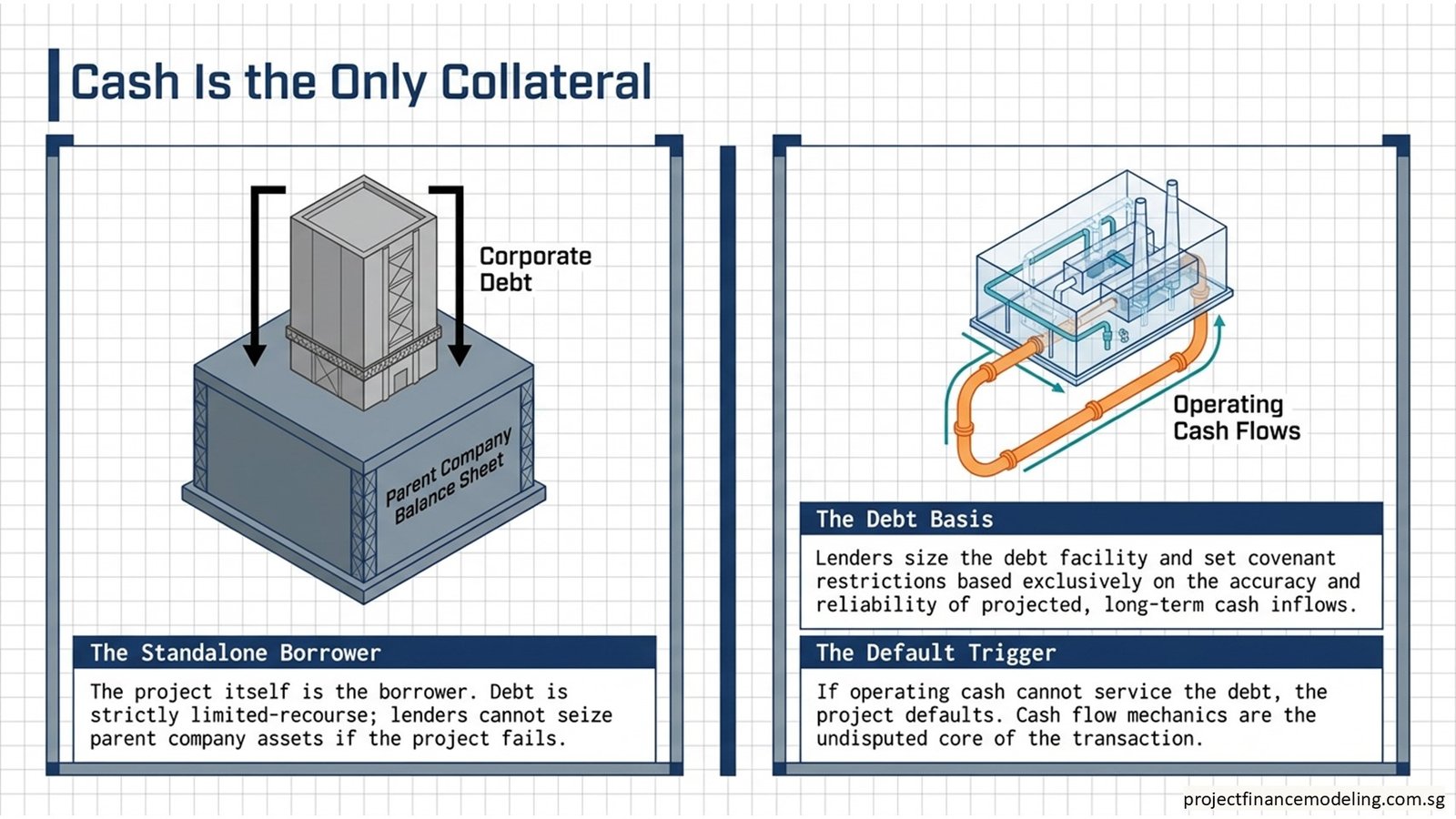

The difference between project finance cash flow modeling and corporate modeling is that the project is the borrower. The debt is not backed up by a parent company’s balance sheet. Since the only way the lenders can get their money back is through the cash that will be generated by the project, the accuracy and reliability of the cash flow model are crucial.

Why Is Cash Flow the Most Important Element in Project Finance Modeling?

In project finance, cash flow is not just another factor to consider but the very core of the deal. Lenders base the size of the debt on expected cash flows. The cash flow ratios are used to set the covenants. Equity returns are the returns on the residual cash flows after all the senior obligations have been satisfied.

The Debt Service Coverage Ratio (DSCR), which compares the lender’s operating cash flow to the total debt service for a specific period, is the most important ratio that the lender looks at. The default provisions are activated when the DSCR is below 1.0x because that indicates that the business cannot provide operating cash to service its debt. The minimum DSCR that lenders may require is between 1.20x and 1.40x based on the project risk level.

All assumptions made in the model eventually end up in the cash flow line and impact the DSCR. Therefore, cash flow mechanics are at the heart of the project finance training provided by professionals.

What Inputs Are Needed Before Building a Cash Flow Projection Model?

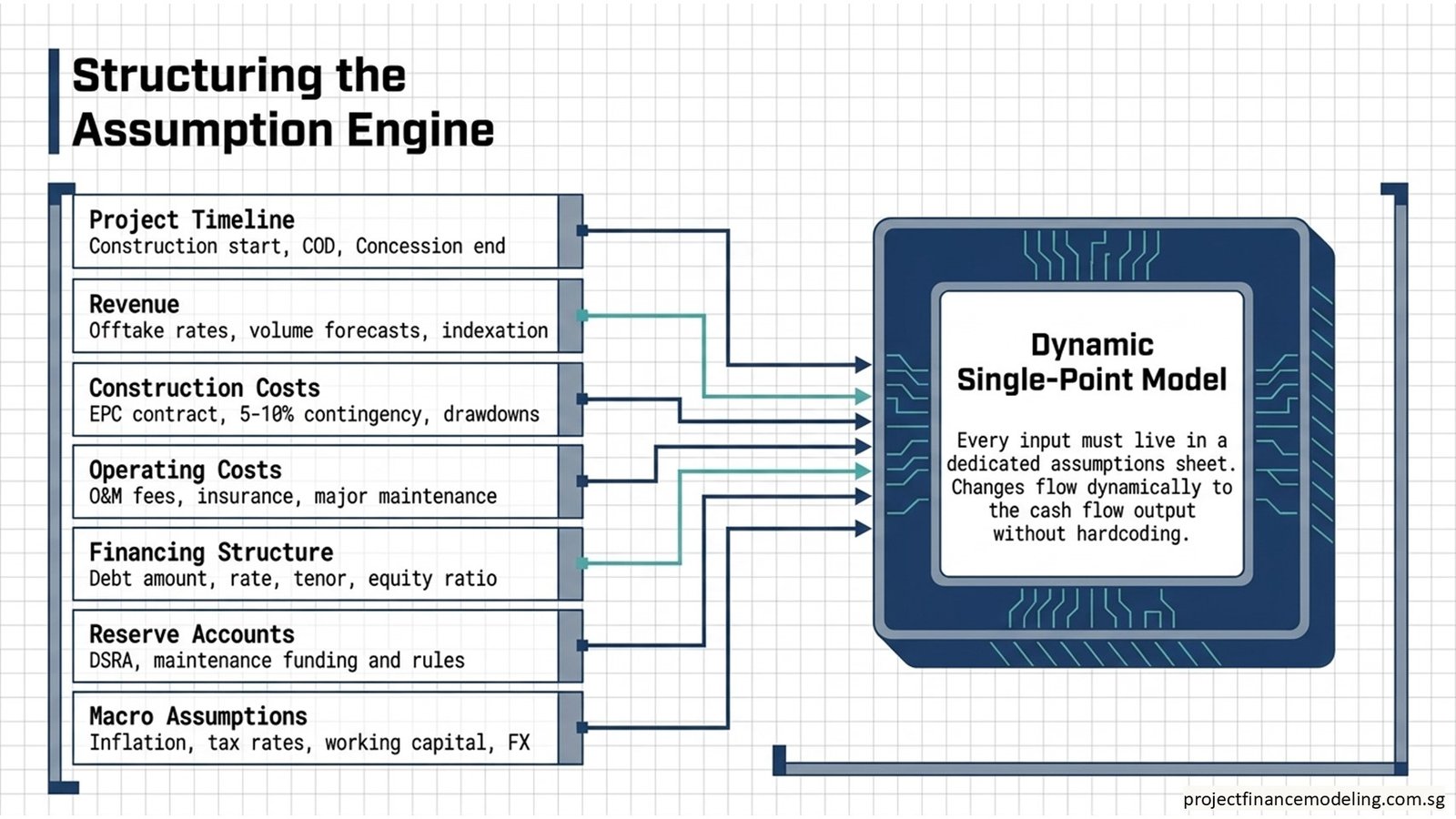

Analysts need to collect and organize multiple sets of inputs prior to the construction of the projection. Every input category has its own block in the model and each of them should be connected dynamically to a block in the cash flow output such that if the input changes, the change should be reflected in the cash flow output automatically.

| Input Category | Key Data Points | Modeling Purpose |

| Project timeline | Construction start period, Commercial operation date (COD), Concession end | Explain the concept of period structure and phase boundaries. |

| Revenue assumptions | Tariff or offtake rates, volume forecasts, indexation clauses | Make up the high line cash inflow forecast. Make up the high line cash inflow forecast. |

| Construction costs | EPC contract value, contingency, payment milestones and drawdown schedule | Simulate construction phase outflows and IDC |

| Operating costs | O&M fees, insurance, land lease, overheads, and the major maintenance cycle | Identify the cash outflows in the operating phase. |

| Financing structure | Debt amount, interest rate, tenor, repayment profile, equity ratio | Organize the obligations on the liability side of the balance sheet and the debt service payments. |

| Reserve accounts | DSRA, major maintenance reserve — funding requirements and release rules | Model ring-fenced cash held for lender protection |

| Macro assumptions | Inflation rate, tax rate, working capital cycle, FX (if applicable) | Adjust Nominal cash flows and tax liabilities |

The first step taken by any analyst before creating any calculations is to put together the inputs in a clearly labeled assumptions sheet. Having a well-documented assumptions document helps the model be transparent, auditable, and keeps it up-to-date in case of changes in assumptions, such as negotiations or the due diligence process progress.

How Are Revenue and Operating Cash Flows Forecasted in Project Finance?

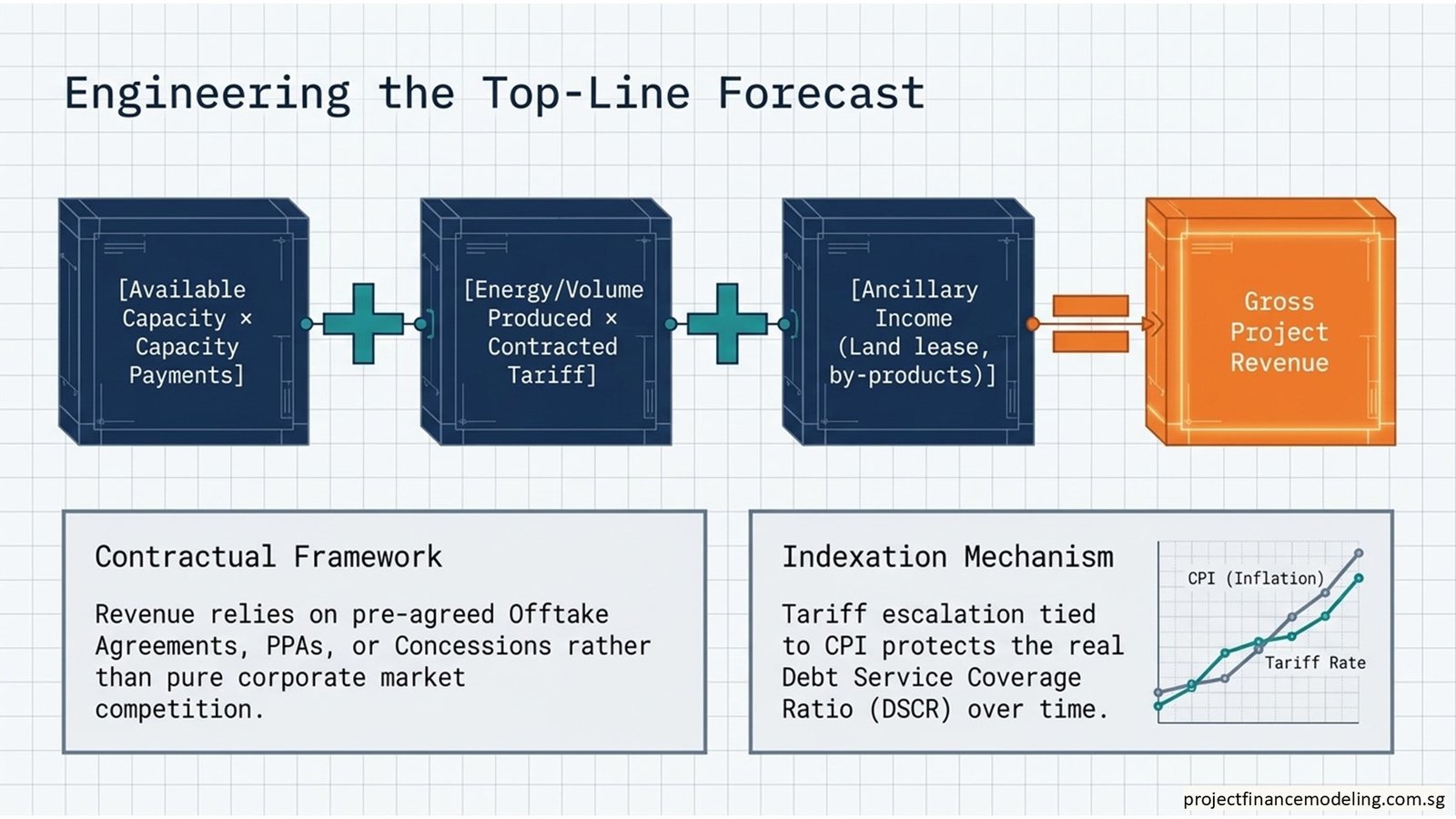

A typical approach to revenue modelling for project finance starts with a contractual/tariff framework, such as an offtake agreement, power purchase agreement (PPA), concession-based tariff, or tolling structure. The asset is made financeable with limited recourse because revenue is generated by project finance and is typically fixed based on a pre-agreement with the project parties, rather than being based on market competition as in corporate models.

Volume assumptions are multiplied by applicable rates to create analysts’ estimates of revenue. This can be defined as available capacity x capacity payments, plus energy produced x the energy tariff for a power project. For a toll road, it is modeled daily traffic volume times the toll rate and then the ramp-up curve for the first 2-5 years of service.

Whereas it is built into the contracts, indexation is included in the tariff escalation. A common method is to index a percentage of the revenue to CPI annually, which offers some protection from cost inflation and maintains the real DSCR consistent over time.

| Cash Flow Category | Type | Examples | Phase |

| Capacity/availability payments | Inflow | Contracted capacity fee from the offtaker | Operations |

| Energy/volume revenue | Inflow | Throughput-based revenue under PPA or tariff | Operations |

| Ancillary income | Inflow | Land lease, by-product sales, bonus payments | Operations |

| EPC contractor payments | Outflow | Construction milestone payments | Construction |

| Operating and maintenance costs | Outflow | O&M contract fees, insurance, overhead | Operations |

| Interest during construction (IDC) | Outflow | Capitalised interest on drawn debt | Construction |

| Debt service | Outflow | Interest + scheduled principal repayment | Operations |

| Reserve account funding | Outflow | DSRA build-up, major maintenance reserve | Operations |

| Equity distributions | Outflow | Residual cash returned to sponsors | Operations |

How Are Construction Costs and Operating Costs Incorporated Into Cash Flow?

The EPC contract is used as the major source of construction costs. A drawdown schedule is created by analysts to link contract milestone payments to the time periods of the models involved. Contingency is usually 5-10% of the EPC value and is posted as an item and is considered available, but is drawn on as and when cost overruns happen.

Interest during construction (IDC) is the interest that is accrued on the total debt drawn at the applicable interest rate for each construction period. Depending on the financing contract, IDC can be capitalised (contributed to the total project investment and funded by extra debt and/or equity) or paid out in advance as it becomes due.

Modeling of operating costs includes both fixed costs and variable costs. For the contract fee for O&M, insurance, land lease and site overhead, the project assumes a rate of inflation on these as fixed costs. The variable costs associated with throughput or volume of production are represented as an output rate. Major maintenance events are either expensed in the model period in which they occur or are funded in a major maintenance reserve account that holds cash in advance for major maintenance events.

How Does Financing Structure Affect Cash Flow Projections?

The financing structure dictates the allocation of debt/equity and how each tranche of financing is used, serviced and repaid. This division has a direct impact on the operating cash flow profile for the entire operating life.

The higher the debt-to-equity ratio, the greater the equity return in favorable situations, and the lower the buffer of the DSCR, the less headroom there is for underperformance. The lender determines the maximum level of gearing (also known as debt service coverage ratio) depending on the risk profile of the project and the minimum requirement for debt service coverage ratio (DSCR) for the loan tenor. The ratio of debt to equity for a typical infrastructure project is between 65:35 and 80:20.

The profile of the cash flows in each period is also very much dependent on the cash flow repayment profile — be it a flat DSCR, a standard annuity, or a bullet repayment. One of the more common methods of structuring debt service in a project finance transaction is to match the debt service with the forecasted revenue, which lessens the risk of a DSCR shortfall during times of lower revenues, like ramp-up.

| Financing Variable | Modeling Impact | Lender / Analyst Focus |

| Debt-to-equity ratio | Higher debt increases DSCR pressure; lower debt reduces equity leverage | Maximum gearing covenant |

| Interest rate | Affects IDC during construction and periodic debt service cost | Base rate + margin; hedging assumptions |

| Loan tenor | Longer tenor reduces annual debt service; extends risk exposure | Typically 15–25 years for infrastructure |

| Repayment profile | Annuity vs sculpted vs balloon; shapes annual cash flow requirements | Minimum DSCR maintenance |

| Debt service reserve account (DSRA) | Funded upfront; absorbs short-term DSCR shortfalls | Typically, 6 months of debt service |

| Grace period/construction drawdown | Debt drawn progressively; interest capitalised during construction | IDC calculation and total debt sizing |

What Is a Cash Flow Waterfall in Project Finance Models?

A cash flow waterfall is the prioritized allocation of operating cash in each period. It determines the order of obligations paid and guarantees that lenders are paid before equity investors are paid.

This allocation logic is applied in a consistent manner throughout all operating periods in every project finance model. The waterfall is more than just a concept — it is a series of Excel calculations that are cascaded through the system and include conditional logic to determine what cash is available at each tier when there is a deficit or surplus.

| Priority | Cash Allocation | Description |

| 1 | Operating expenses | O&M costs, insurance, taxes, and site overhead are paid first from revenue |

| 2 | Debt service reserve account top-up | Keep the debt service ratio at the desired level prior to the debt service. |

| 3 | Senior debt interest | Interest on the unpaid principal balance of the senior loan. |

| 4 | Senior debt principal | The principal amount due is based on the amortisation schedule. |

| 5 | Major maintenance reserve funding | Save money to cover significant maintenance activities |

| 6 | Junior debt service (if applicable) | Interests and principal on mezzanine or subordinated debt. |

| 7 | Equity distribution | The net cash that sponsors have left over after all senior obligations have been satisfied. |

In reality, the waterfall also contains cash sweep provisions — provisions which require that any cash in excess of a certain DSCR threshold be used for accelerated debt repayment, instead of equity distribution. The allocation rules are enforced dynamically for all model time periods by using a nested IF statement and running balance calculations in the Excel spreadsheet where the waterfall model is built.

How Is Debt Service Modeled in Cash Flow Projections?

Debt service can be broken down into two parts: interest payments on the outstanding loan amount and regular principal repayments. Each must be computed on an individual basis and then added together to obtain the total debt service in any given period.

Interest is the amount of the loan balance outstanding on the first day of the interest period at the interest rate for the period. Principal repayment is based on the amortisation profile selected, which can be annuity, straight-line or sculpted. For a sculpted profile, the analyst starts with a desired DSCR and calculates the amount of principal that can be paid in each period based on the projected operating cash flow.

Divide operating cash flow available for debt service by total debt service to get the DSCR. As the lender monitors both, analysts usually calculate both the annual DSCR and the project life coverage ratio: the ratio of remaining project NPV to remaining debt.

How Do Analysts Handle Timing Differences in Cash Inflows and Outflows?

One of the most challenging parts of project finance cash flow is timing. An offtake agreement may be used to receive revenues quarterly and costs monthly. Some calendar dates may be set for debt service that don’t correspond to the dates that revenues are received. The working capital, or the difference between the time costs put into the business and when the cash is recovered, should be clearly represented.

These timing differences are addressed by the analyst using a consistent time period basis for the infrastructure model (e.g., semi-annual or annual models for long-term infrastructure) and working capital assumptions that reflect the actual payment terms of the project contracts. A receivables cycle of 30 days, with quarterly billing, for instance, causes a predictable and measurable cash timing gap, which means less cash to pay debt in any quarter.

Another important timing risk is construction delay. The six-month delay in the commercial operation date will cause a six-month shift of revenues, will lengthen IDC, and could result in construction loan milestone default. This is explicitly included in the scenario analysis block and considered by analysts in determining the impact on the DSCR and financial viability of the project.

How Is Net Cash Flow Calculated Step by Step in Project Finance Models?

Net cash flow is the ultimate end result of the projection and the net result at the end of each layer of the waterfall, including costs, reserves, and debt service, which is the available cash flow for equity.

| Step | Activity | Model Output |

| 1 | Build the project timeline and period structure | Semi-annual or annual periods from financial close to concession end |

| 2 | Input and link all assumptions to a dedicated assumptions sheet | Single point dynamic model (input change) |

| 3 | Model revenue by volume and rate assumptions with indexation | Gross revenue forecast by period |

| 4 | Model operating costs by fixed and variable components with escalation | Total operating expenses for the period. |

| 5 | Calculate EBITDA as revenue minus operating costs | Funds available for debt service (cash flow) |

| 6 | Build the debt drawdown schedule and IDC during construction | Cumulative debt balance and total project cost |

| 7 | Build the debt amortisation schedule and interest calculations | Total debt service by period |

| 8 | Apply the waterfall: deduct reserves, interest, principal in sequence | Cash available for equity distribution for each period |

| 9 | Calculate DSCR, LLCR, and PLCR for each period | Coverage ratio outputs for lender covenant testing |

| 10 | Run scenario and sensitivity analysis on key assumptions | Range of DSCR results for base-case, stress conditions and optimistic conditions. |

How Do Sensitivity and Scenario Analysis Improve Cash Flow Accuracy?

The sensitivity analysis shows the impact on the DSCR and equity returns by varying one of the assumptions — revenue, operating costs, inflation, construction delay, or interest rates. One way sensitivity table may present changes in the minimum DSCR with the different revenue tariffs ranging from 80% to 120% of the base case assumption. This will indicate lenders how much the project may experience in terms of revenue loss before defaulting on the debt service covenant.

The key feature of scenario analysis is to create complete scenarios (base case, upside, downside, stress), which adjust several assumptions at the same time. A plausible adverse combination includes a six-month construction delay, a 10% cut in revenues and a 5% rise in operating costs.

Experts taking a structured project finance modeling course learn how to create and use these analyses effectively in Excel, and how to use the data tables and scenario managers to generate the output that lenders and investment committees are able to review and interrogate directly.

What Are Common Mistakes in Project Finance Cash Flow Modeling?

The most common modelling mistake is to enter the value into the model by hand when it should be connected to the assumptions sheet. If interest rates, inflation, or tariff rates are hardcoded into the cells that calculate them, the model will be hard to update and may have inconsistent errors during scenario runs.

Another frequent error is not staying on top of the distinction between cash and accounting items. Depreciation is a non-cash expense that lowers taxable income, but does not lower cash debt service. Capitalised IDC is not an expense, but rather a cash outflow that occurs during construction, which is not called an expense and is listed on the balance sheet. Any analyst who mixes them up skews a company’s DSCRs either up or down from what the debt service capacity really is.

There are many errors in timing, especially during transitions from construction to operations. If the commercial operation date is not properly dealt with, revenues and operating costs may start in the wrong year, significantly affecting the first year’s DSCR. In long-tenor models, small errors in period boundaries accumulate over years and result in significant errors in the outcome.

Conclusion

Project finance cash flow projection is a sequential and structured process that starts with the project timeline and assumptions, continues through the revenue and cost forecast, the financing structure and debt service schedule, and ends with the waterfall allocation that determines the funds available for the equity investors.

All the steps are linked together. Operating cash flow is impacted by the revenue tariff, which impacts the DSCR, which may necessitate a change in the debt amortisation profile, which will impact the equity return. The understanding of these interdependencies – and appropriate modelling in Excel – is the fundamental skill mastered by project finance practitioners through practice and systematic training.

The number that lenders will be looking at the most closely is the DSCR, and it is solely generated by the cash flow model. Analysts with a strong ability to construct a sound, verifiable and adaptable cash flow model can make valuable contributions to financing infrastructure transactions, developing energy projects, and structuring longer-term capital markets transactions.

Whether you are taking a project finance modeling course or developing a career in infrastructure finance, cash flow mechanics is a topic that should be learned first and foremost, as all other topics of infrastructure finance are built on top of it.

| Concept | Key Modeling Takeaway |

| Cash flow waterfall | Applies the cash assigned for operations in the correct order: from costs to equity distributions |

| DSCR | Operating cash flow divided by total debt service; primary covenant metric for lenders |

| Revenue modeling | Built from volume drivers and contracted rates, indexation links tariffs to inflation |

| IDC | Interest capitalised during construction – adds to the total project cost and demands the debt. |

| Sculpted debt service | Common in infrastructure financing, principal payments are sized to keep a target DSCR. |

| Sensitivity analysis | Tests how the DSCR reacts to changes in one of the variables; sets the lender’s risk tolerance |

| Scenario analysis | Aggregates several negative assumptions and tests the financial viability of the project |

| Common mistakes | The confusion of hardcoded inputs, cash vs accounting, and construction-to-operations timing errors. |

The skills you learn in a structured project finance training programme are most directly applicable to the finance discipline – cash flow modelling skills are the most applicable to everyone from the analyst starting their first infrastructure model, to the banker reviewing a project loan, to the developer working on a financial close package.